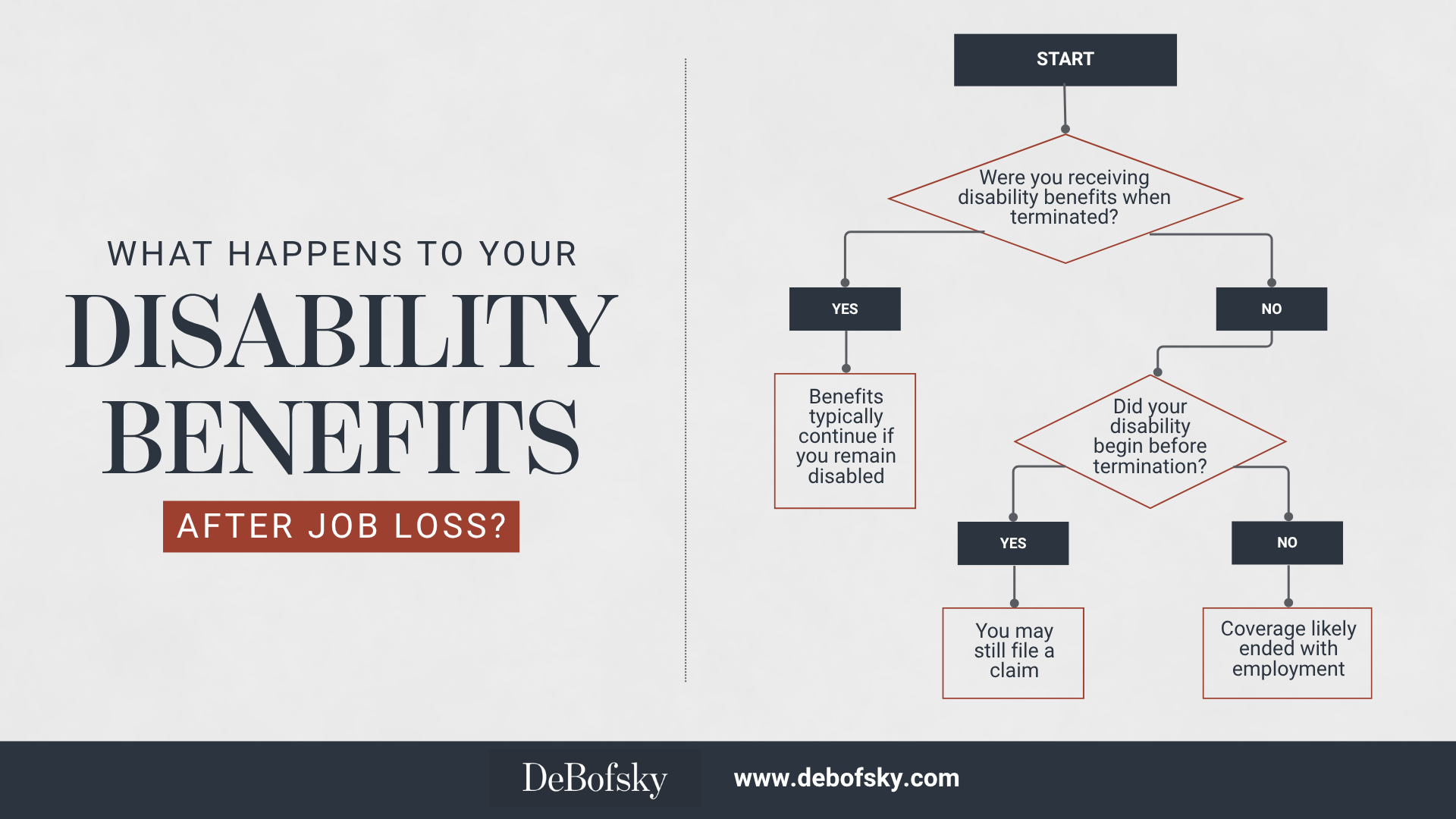

Many employees worry about losing disability benefits after job termination. The short answer: you can often continue receiving benefits after losing your job. What matters is when your disability began, not whether you remain employed.

Before exploring this topic, you need to understand how disability benefits differ from job-protected leave. The Family and Medical Leave Act (FMLA) protects your job for up to 12 weeks. FMLA leave is unpaid. Disability benefits replace a portion of your income, typically 50% to 70% of earnings. Your employer provides these benefits through private insurance policies. These protections serve different purposes and follow different rules.

Key Takeaways

- You can often continue receiving disability benefits after termination. What matters is when your disability began.

- FMLA protects your job for 12 weeks. Disability benefits replace income. These are separate protections.

- Most long-term disability recipients eventually lose their jobs. Benefits typically continue until retirement age if you remain disabled.

- Employers cannot fire you to prevent you from filing a disability claim. Section 510 of ERISA prohibits this interference.

- You have 180 days to appeal a denied ERISA disability claim. Missing this deadline can permanently end your case.

Table of Contents

Disability Benefits and Job Termination: What You Need to Know

Download the Infographics here

What Happens to Long-Term Disability Benefits After Job Loss?

Yes, you can continue receiving disability benefits after your employer terminates you. This outcome is not unusual. Most people who receive long-term disability benefits for more than a few months eventually lose their jobs. Long-term disability plans typically pay benefits until retirement age. The key requirement: you must remain disabled under the policy’s definition.

Some plans exclude coverage if the employer terminates you “for cause.” This means gross misconduct. However, these provisions are rare. Request a copy of your plan document to understand your ERISA rights.

Courts also recognize the reality that disabled employees face. Most employees cannot simply quit their jobs. Their paycheck is their main or sole income source. They push through their symptoms until they physically cannot continue. The Sixth Circuit addressed this in Rochow v. Life Ins. Co. of N. Am., 482 F.3d 860 (6th Cir. 2007). The court held that insurers cannot deny a claim solely because the claimant kept working after symptoms began.

Does Being on Disability Protect My Job?

No. Receiving disability benefits does not protect your job. Many employers terminate employees after they receive long-term disability benefits for several months. Employers reason that the employee will not return to work anytime soon. They also need to fill the position. For more on this topic, see our article on disability benefits after FMLA or employment termination.

However, a critical legal distinction exists. An employer can terminate someone already receiving benefits. An employer cannot terminate someone to prevent them from filing for benefits. Section 510 of ERISA prohibits this interference. You can sue your employer if they fired you to block your access to benefits. Section 510 also protects employees who face retaliation for attempting to access benefits.

Do Disability Payments Continue After Termination?

In most cases, yes. Disability payments continue after termination. Some policies state that employees lose eligibility if terminated “for cause.” Review your specific policy language. A for-cause termination may affect your benefits, but these provisions remain uncommon. Learn more about when disability benefits can be terminated.

Your health insurance coverage will also change after termination. Employer-sponsored healthcare typically ends on the last day of the month you were terminated. You can elect COBRA continuation coverage to maintain your insurance. This matters because you must continue providing proof of disability. Ongoing medical treatment supports your claim.

If COBRA costs too much, explore options at healthcare.gov. Maintaining treatment documentation is essential even without employer-sponsored coverage. Gaps in medical evidence can jeopardize your ongoing benefits.

Have you been terminated while receiving disability benefits? The timing of your termination matters. If your employer fired you to prevent you from accessing benefits, you may have legal recourse under ERISA Section 510.

Contact DeBofsky Law to discuss your situation

Can I Get Short-Term Disability After Being Fired?

Short-term disability (STD) benefits replace income when illness or injury prevents you from working. These benefits cover non-work-related conditions. Employers are not required to provide STD, but many do. Benefit duration varies by policy. Some plans pay for several weeks; others pay for up to one year. For more, see our article on short-term disability and job protection.

If your employer terminates you before you file an STD claim, expect resistance. The insurer may scrutinize your application more closely. However, if your disability began while you were still employed and covered, you may still qualify.

Unlike FMLA, short-term disability does not protect your job. You can be fired while on STD leave. The Americans with Disabilities Act (ADA) may provide some protection. The ADA requires employers with 15 or more employees to offer reasonable accommodations. Some states require accommodations from smaller employers. Illinois, for example, requires employers with even one employee to accommodate disabilities. A temporary leave request may qualify as a reasonable accommodation if it does not cause “undue hardship.” For accommodations, visit askjan.org. However, if you cannot return to work, your employer may eventually terminate you.

If you face this situation, consult an experienced employee benefits attorney. You may still qualify for benefits despite losing your job. You may also have a claim against your employer if they fired you to block your benefits.

Return-to-Office Mandates and Disability Benefits

Since 2023, many employers have implemented strict return-to-office (RTO) policies. Employees with disabilities may face termination if they cannot comply. If you were working remotely due to a disability and now face termination over an RTO mandate, your situation involves complex legal issues. RTO policies can intersect with ERISA disability benefits, ADA accommodations, and employer interference claims. We address this emerging issue in our article on return-to-office mandates and ERISA disability termination.

Can My Employer Fire Me if My Disability Claim Is Denied?

No. Your employer cannot fire you for exercising your right to apply for disability benefits. This remains true even if your claim is denied. Firing you for filing a claim constitutes unlawful interference with benefits. ERISA Section 510 (29 U.S.C. § 1140) prohibits this conduct. State laws also protect employees as a matter of public policy.

However, other rules still apply. If you have been on leave for more than 12 weeks in a 12-month period, FMLA no longer protects your job. Your employer may terminate you for excessive absences. Learn how to protect yourself in our guide on avoiding job abandonment when claiming disability benefits. This applies whether your disability claim is approved, denied, or still pending.

The key question: why did your employer fire you? If the answer is “because you filed a disability claim,” you have a cause of action. Learn more about the importance of ERISA claim appeals.

Can I Collect Unemployment if Terminated While on Disability?

Yes, you can collect unemployment while on disability. However, doing so is not always wise.

First, your disability policy likely treats unemployment benefits as deductible income. The insurer will offset your disability payments by the unemployment amount. You may gain nothing by collecting both.

Second, unemployment agencies require you to certify that you are “ready, willing, and able to work.” This statement contradicts your disability claim. If your insurer discovers you are collecting unemployment, they may use this against you. They could argue you are not credible or not truly disabled.

That said, sometimes unemployment makes sense. If your STD or LTD application has been denied and you are appealing, you need income. If your application remains pending, you may face months without pay. In these situations, apply for both. Understand that you may need to repay your disability insurer for any overpayment.

Can I Apply for Disability Benefits While Still Employed?

Yes. You can apply for disability benefits while still working. Request an application from your employer or plan administrator. Complete it along with a questionnaire from your doctor. For the onset date, select a future date when you expect to stop working. For step-by-step guidance, see our article on the five steps to applying for long-term disability benefits.

Working while filing a claim does not automatically disqualify you. Courts have recognized this reality. The Seventh Circuit explained it clearly in Hawkins v. First Union Corp. Long-Term Disability Plan, 326 F.3d 914, 918 (7th Cir. 2003). The court noted there is no “logical incompatibility between working full time and being disabled from working full time.” A desperate person might force themselves to work despite a totally disabling illness.

Plan ahead for the timing. If ERISA governs your benefits plan, the plan administrator has 45 days to decide your claim. They can extend this deadline twice, each time by up to 30 days. The maximum total decision period is 105 days. To avoid an income gap, apply at least 105 days before you plan to stop working. If your insurer delays your claim beyond these deadlines, you may have legal options.

A Note on State Paid Family and Medical Leave Programs

Many states now offer paid family and medical leave (PFML) programs. These state-mandated programs provide wage replacement during leave. They operate separately from employer-sponsored disability plans.

State PFML programs are not governed by ERISA. Different rules and appeal processes apply. If you have questions about state-mandated programs, contact your state labor department.

This article addresses employer-sponsored short-term and long-term disability benefits. These plans typically fall under ERISA, which means specific federal procedures govern claims, appeals, and lawsuits.

Protecting Your Disability Benefits During and After Employment

Understanding your rights is the first step. Taking timely action protects your benefits.

If You Are Currently Employed and Considering a Disability Claim:

Apply before you stop working if possible. Plan for the 105-day maximum decision period under ERISA. Document your symptoms and limitations. Continue medical treatment and keep records.

If You Have Been Terminated While Receiving Benefits:

Your benefits should continue if you remain disabled. Review your policy for for-cause termination provisions. Maintain your medical treatment despite losing employer-sponsored insurance. COBRA or healthcare.gov coverage can help.

If Your Disability Claim Has Been Denied:

Do not ignore the denial. You have 180 days to appeal under most ERISA plans. The appeal is your one chance to build the evidentiary record. Request your complete claim file. Address each reason for denial with new evidence.

If You Suspect Your Employer Fired You to Block Your Benefits:

Document the timing and circumstances. ERISA Section 510 prohibits interference with employee benefits. You may have grounds for a lawsuit against your employer.

When Legal Help Makes Sense

Not every situation requires an attorney. But employer-sponsored disability claims involve complex federal procedures. The appeal deadline is strict. The administrative record is often all a court will review. Mistakes during the appeal can permanently limit your options.

DeBofsky Law focuses exclusively on ERISA and disability insurance disputes. We represent physicians, attorneys, executives, and other professionals whose employer-sponsored benefit claims have been denied.

We do not handle Social Security disability, workers’ compensation, or state-mandated leave programs. If your situation involves an employer-sponsored plan denial, we can help.

Frequently Asked Questions About Disability Benefits and Job Termination

Can My Long-Term Disability Benefits Continue After I Am Fired?

Yes. Your long-term disability benefits can continue after your employer terminates you. Losing your job does not automatically end your right to benefits.

What matters is when your disability began. If you became disabled while covered under the policy, you likely remain eligible. Most long-term disability plans pay benefits until retirement age, regardless of employment status. In fact, most people receiving LTD benefits for more than a few months eventually lose their jobs. Continued benefits after termination is the norm, not the exception.

Review your policy for “for cause” termination provisions. Some policies exclude coverage if your employer fires you for gross misconduct. These provisions are uncommon, but they exist. Request your plan document to confirm your rights.

Can My Employer Terminate Me to Prevent Me From Filing a Disability Claim?

No. Your employer cannot legally fire you to prevent you from filing a disability claim. This conduct violates federal law.

Section 510 of ERISA specifically prohibits employer interference with employee benefits. If your employer terminated you to block your access to disability benefits, you can sue them. Section 510 also protects you from retaliation for attempting to access benefits you earned.

The timing and circumstances of your termination matter. If you announced you needed to file a disability claim and your employer immediately fired you, that timing suggests interference. Document every conversation. Save emails and written communications. An experienced ERISA attorney can evaluate whether your termination violated Section 510.

How Long Do I Have to Appeal a Denied Disability Claim?

For employer-sponsored plans governed by ERISA, you typically have 180 days to file an administrative appeal. This deadline is strict and starts when you receive the denial letter.

Missing this deadline can permanently waive your right to challenge the denial. You may lose access to federal court entirely. The appeal is also your only opportunity to build the evidentiary record. Courts reviewing ERISA cases generally consider only evidence submitted during the appeal.

Do not wait to act. Request your complete claim file from the insurer. Review the stated reasons for denial. Gather additional medical evidence. Consider consulting an ERISA attorney before filing. For more, see our article on LTD benefits denial and appeals.

Does Losing My Job End My Disability Insurance?

No. Losing your job does not automatically end your disability insurance benefits. Your eligibility depends on when your disability began, not your current employment status.

If you became disabled while covered under your employer’s plan, you may still qualify for benefits. Think of it like car insurance: what matters is whether you had coverage when the accident occurred, not whether you still have the policy today.

However, if you were not disabled before termination and then became disabled afterward, you typically cannot file a claim. The coverage ended with your employment. This distinction is critical for understanding your rights.

Can I Apply for LTD Benefits After Being Terminated?

Yes, if your disability began while you were still employed and covered. You can file for long-term disability benefits after termination, provided your disabling condition started during your coverage period.

ERISA prohibits insurers from administering claims in ways that “unduly inhibit” benefit applications. Requiring you to apply before termination, when many disabilities prevent working, would violate this standard.

Act promptly after termination. Gather medical records documenting when your condition began. File your application even if you no longer work for the employer. The insurer must evaluate your claim based on when the disability started, not when you applied.