If you have an employment-related benefit claim, ERISA is likely in the picture and presents unique challenges unlike claims such as those involving auto or homeowner’s insurance. ERISA claims involve complex rules and strict deadlines that can be challenging to navigate. Understanding the process can significantly improve your chances of success. This guide outlines how to file a claim, respond to a denial, and improve your chances of winning an ERISA claim or ERISA appeal.

What Is ERISA?

The place to start is to explain what ERISA is. ERISA is an acronym for the Employee Retirement Income Security Act, a law passed by Congress in 1974 aimed at protecting the rights of employees who participate in their employers’ benefit plans and their dependent or named beneficiaries. ERISA applies to a wide range of employee benefits – pensions, 401(k) and 403(b) plans (non-profit and government employees), disability, health, and life insurance benefits, along with severance and other benefits administered by employers.

ERISA’s scope only encompasses the private sector, though. State, federal, or municipal employees are excluded except where they have union-sponsored benefits. Another significant exemption are “church plans,” which are benefits sponsored by religious organizations.

What Is an ERISA Claim?

Just about any type of claim for benefits brought under a private sector or union sponsored employee benefit program is considered an ERISA claim.

ERISA claims encompass several categories, each with specific requirements:

- Disability Benefits: Both short-term and long-term disability claims

- Health Insurance: Medical treatments, medical devices, mental health services, prescriptions

- Life Insurance: Death benefits and accidental death coverage

- Retirement Benefits: Pension and 401(k)/403(b) distributions

- Other Benefits: Severance, supplemental insurance, wellness programs

How Can I Determine My Rights to Bring an ERISA Claim?

Federal law requires that employers provide employees with a summary plan description of their benefit programs. By law, the summary description must include information about claims and how to go about submitting a claim for benefits, deadlines for submitting claims, and claim appeals.

How Do I File an ERISA Claim?

Different types of claims may utilize different claim procedures. To the extent an employee is uncertain as to their rights after reviewing the summary plan description for the benefit at issue, human resources personnel should be able to explain the process.

Here are some specifics as to different types of claims:

Retirement Benefits

Depending on the nature of the retirement benefits claim (i.e., pension or 401k/403(b)), employees typically need to complete a set of forms specifying how and to whom benefits are to be paid. For retirement, once an election is made, it is usually irrevocable. So, the employee should understand and make sure they are making the correct election. The employee may need assistance from a financial advisor. If the employee is married and seeks a lump sum benefit distribution, he or she must submit a notarized written spousal consent.

Disability

There are three parts to every disability insurance benefit claim that must be completed and submitted — the employee’s statement, the employer’s statement, and the attending physician’s statement.

Employee Statement

The employee’s statement describes the nature of the disabling impairment and how it affects the employee’s ability to work. When completing the employee statement, the claimant should be specific about how their condition affects their ability to function at work. Instead of simply stating “I cannot work,” the employee should describe exactly which job duties cannot be performed and why. For example: “Cannot type for more than 15 minutes continuously due to carpal tunnel syndrome causing severe pain and numbness” or “Cannot maintain concentration for more than 30 minutes due to pain and medication side effects including drowsiness and confusion.”

Employer Statement

The employer’s statement provides information about the employee’s work duties, when the employee ceased working, and the employee’s rate of pay. It does not as the employer to offer an opinion as to the employee’s disability. HR should also provide a comprehensive job description that includes:

- all physical requirements (lifting, sitting, standing, walking),

- mental and cognitive demands (concentration, multi-tasking, decision-making), and

- environmental factors and stress levels, deadlines, travel requirements.

Physician’s Statement

Finally, the attending physician’s statement explains the nature of the employee’s medical condition and offers other medical information that is used to determine disability. This is a critical document, and the claimant should work closely with their physician to ensure they:

- List specific diagnoses with ICD-10 codes

- Document objective findings from examinations and tests

- Clearly state work restrictions and limitations

- Explain how the employee’s condition prevents the performance of specific job duties

- Include treatment frequency and prognosis

Health Benefits

Most health insurance benefits claims are routine and are submitted directly by the doctor or hospital to the insurer or plan administrator. However, claims that require pre-approval or claims involving newly developed drugs or treatments, and many types of behavioral health treatment, may require a letter of medical necessity from the treating doctor before the claim is approved. Claimants should be sure that their physicians are ready and willing to back up their claims. With certain pharmaceuticals and medical devices, the manufacturer may also be able to provide helpful resources.

Life Insurance or Accidental Death Insurance

In most instances, all that is necessary to complete an application for life insurance benefits is proof of beneficiary designation, a copy of the official death certificate, and completion of a form. The form needs to list the name, address, and other demographic information from the beneficiary claimant. However, if an autopsy was performed, it can be useful to have a copy of the report if available prior to submitting a life insurance claim. In accidental death benefits claims where there was law enforcement involvement, such as a fatal car accident, it would be advisable to obtain a copy of the police report and submit it with the claim.

What Happens After the Claim Is Submitted?

The Insurance company or designated benefits personnel will review the claim. Depending on the nature of the claim, the insurer or plan administrator is required to process the claim within deadlines imposed by the U.S. Department of Labor for rendering a claim decision. Delays may occur if the insurer or benefit administrator needs to gather additional evidence such as medical records, police reports, and medical examiner/coroner evidence.

Common Reasons Why ERISA Claims Are Denied

Understanding why claims are denied can help you build a stronger initial claim:

- Insufficient Medical Evidence – This is the most common reason for claim denials. Insurers often claim that medical records fail to adequately document the severity of the condition or its impact on work ability.

- Definition of Disability Not Met – Many policies have different standards for “own occupation” versus “any occupation.” Understanding your policy’s specific language is crucial.

- Pre-Existing Condition Exclusions – Conditions that were identified or treated during what is known as the “lookback period” before coverage began may be excluded.

- Lack of Appropriate Treatment – Insurers may deny claims if they believe the claimant is not following recommended treatment or not seeing appropriate specialists.

- Surveillance or Social Media Contradictions – Insurance companies may conduct surveillance or review social media posts that appear to contradict claimed limitations.

What Happens if the Claim Is Denied?

If the insurer denies your claim, the claimant has the right to a “full and fair review” of the claim denial. That means the participant or beneficiary has the right to appeal the denial and in fact may be obligated to do so as a prerequisite to seeking court intervention. Many types of claims have very short time deadlines for appeals such as health insurance claims classified as “urgent,” i.e., where the patient’s life is in jeopardy, or the patient is in severe pain. Appeal deadlines in such matters can be as short as three days under federal regulations (29 CFR § 2560.503-1).

Understanding the ERISA Appeals Timeline

ERISA claim appeals are often complex because they may involve medical judgments or legal interpretations. A comprehensive set of regulations issued by U.S. Department of Labor outlines the requirements for appeals, including deadlines imposed both on claimants and on the insurer or plan administrator. Those regulations are intended to ensure the appeal process is fair to the claimant and not treated as a mere rubber stamp.

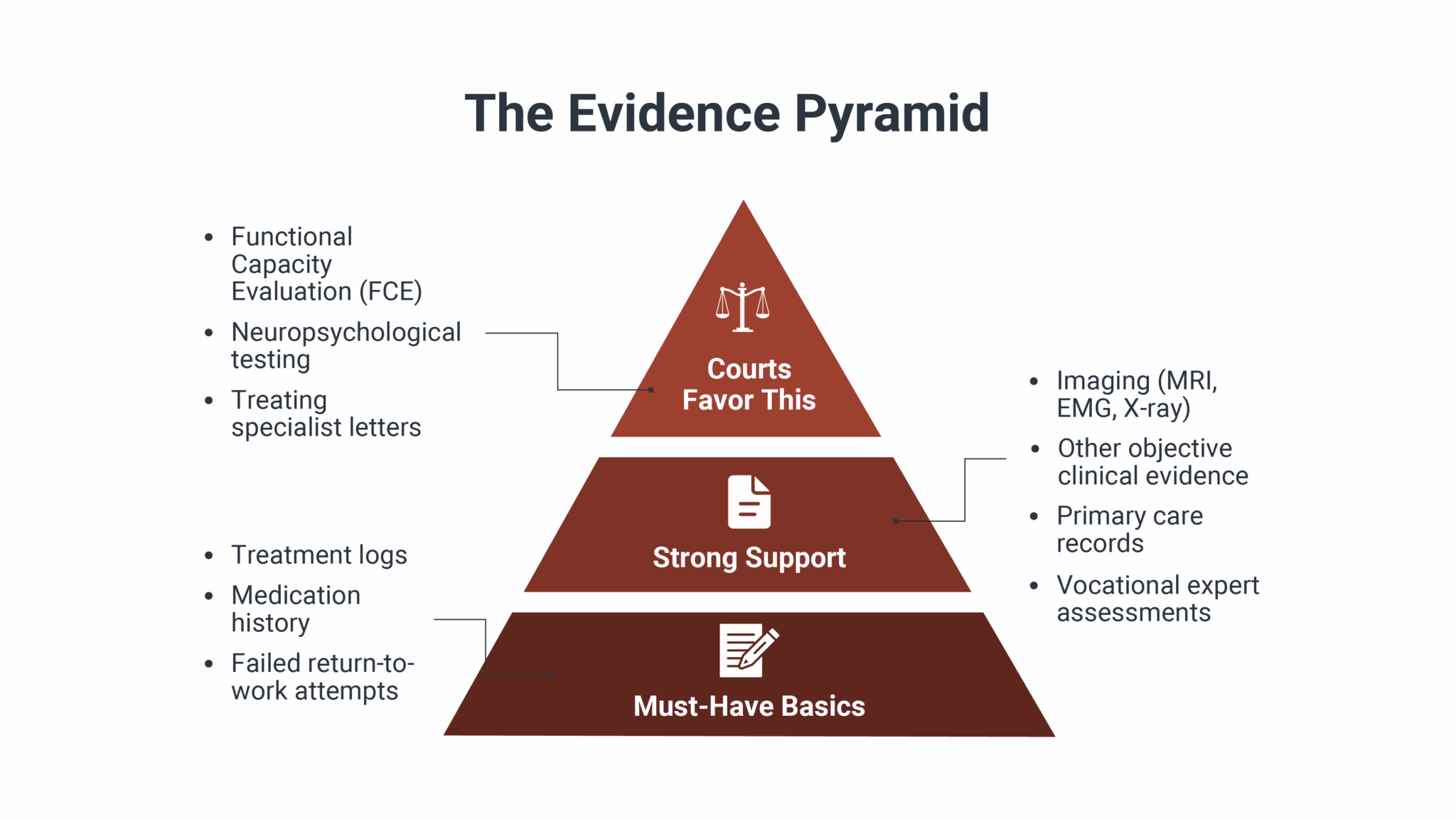

Critical Deadlines You Need to Know about ERISA Disability Claims

The federal regulations establish strict timelines that apply to all ERISA disability claims:

- Initial Claim Decision: The plan has 45 days to decide your claim, with possible extensions up to 30 days (then another 30 days) if matters beyond their control prevent a timely decision. Maximum total time: 105 days.

- Appeal Deadline: If denied, you have exactly 180 days from receiving the denial notice to file your appeal. This deadline is absolute, filing even one day late permanently bars your claim.

- Appeal Decision: Once you file your appeal, the plan has 45 days to decide, with one possible 45-day extension for special circumstances. Maximum total time: 90 days.

- Lawsuit Deadline: If your appeal is denied, you must file in federal court within the contractual limitation period specified in your plan—typically three years from when proof of loss was due, but some plans allow as little as one year.

ERISA appeals involve legal proceedings that often require an attorney’s help. Claimants need assistance to navigate the complex ERISA appeal process. A knowledgeable ERISA attorney will analyze adverse evidence, gather necessary additional evidence, and present winning arguments to overturn unjustified denials. Early attorney involvement is crucial because if an appeal is unsuccessful, courts may not consider new evidence later. Waiting until after a claim appeal is denied to hire an attorney could preclude a successful lawsuit.

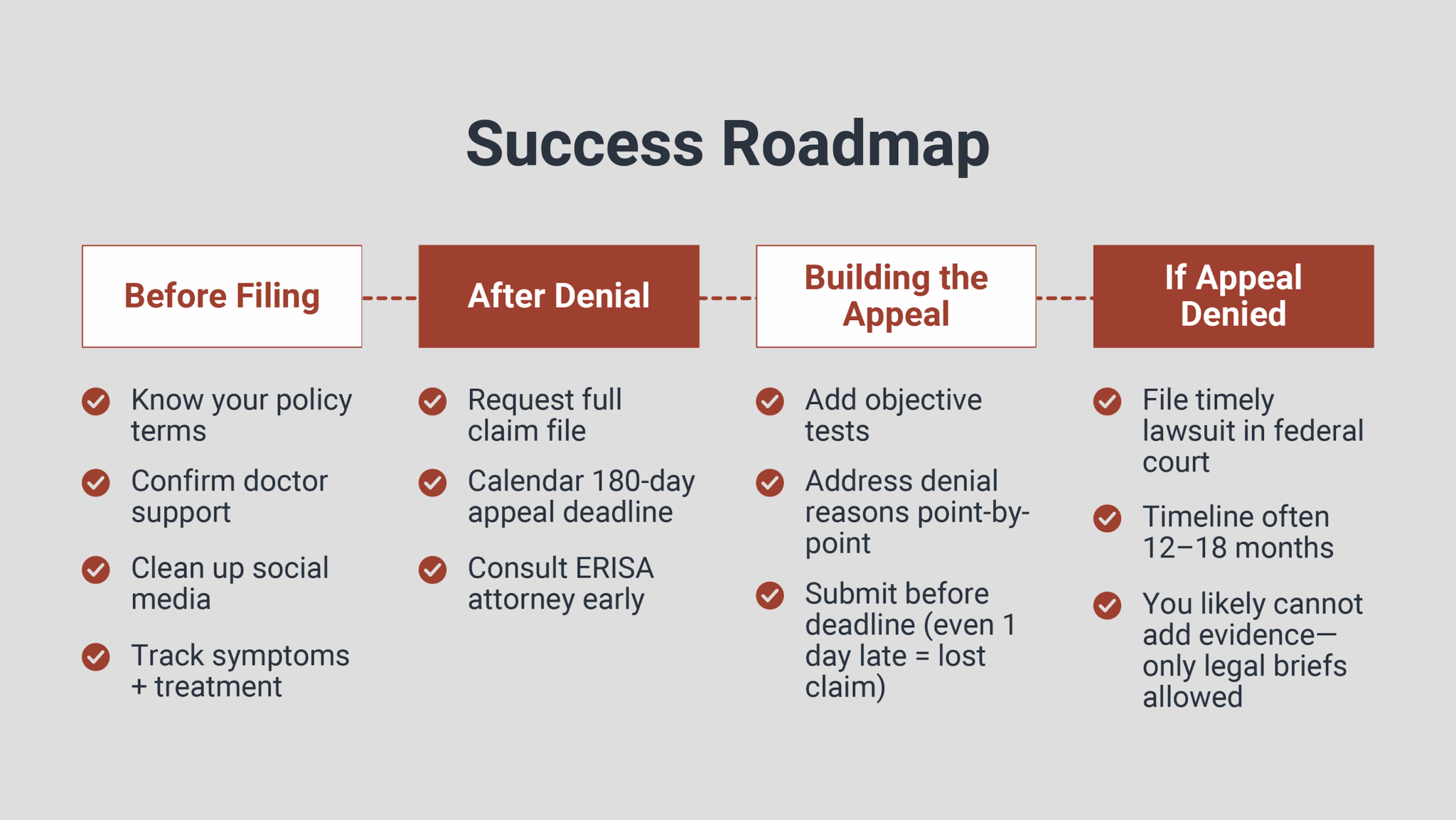

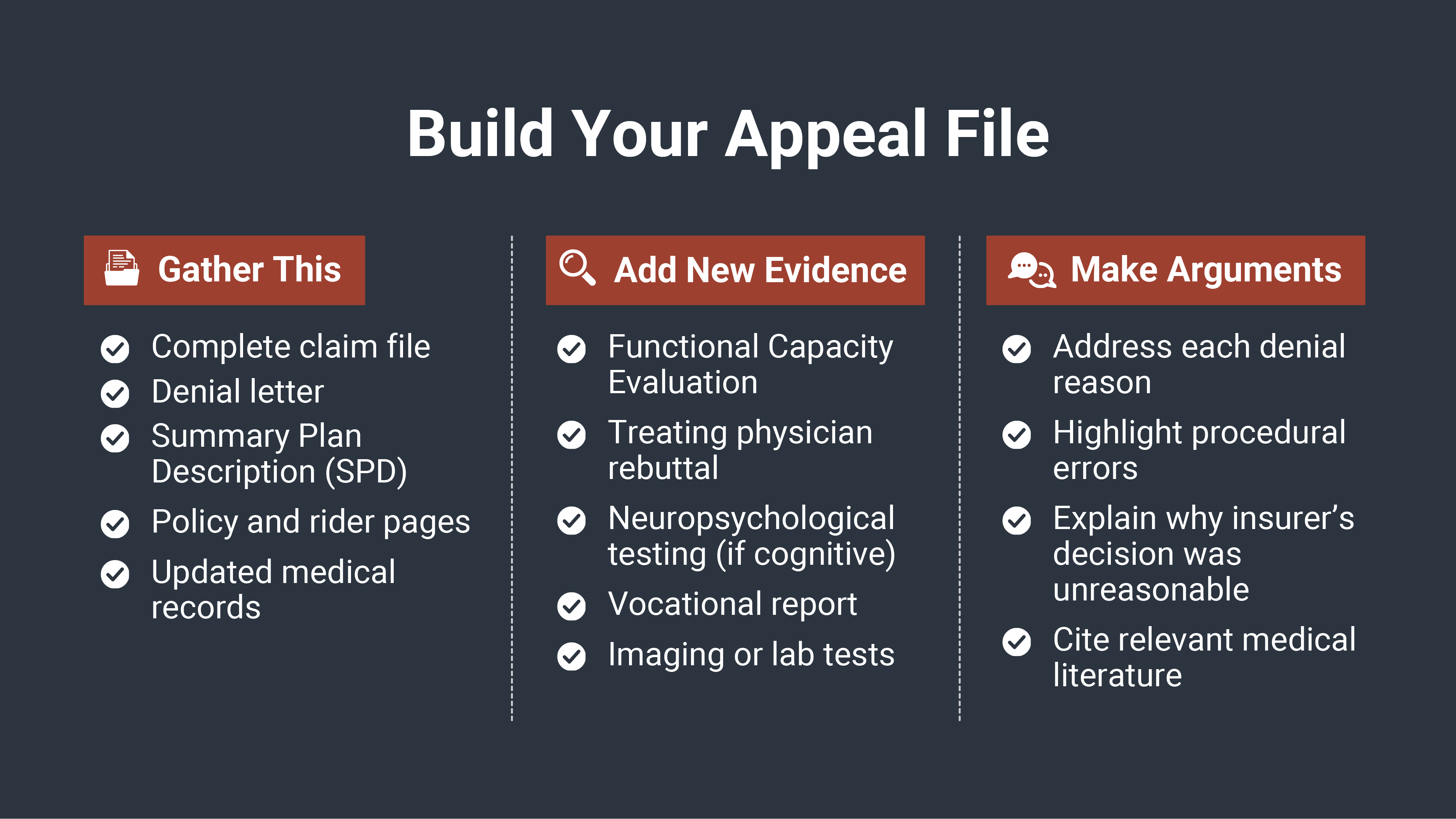

Building a Strong Appeal

1. Request Your Claim File: Under ERISA, you have the right to review all documents the insurer used in their denial decision. Request this immediately – by law, the claimant should receive the claim file within 30 days at no charge (29 CFR § 2560.503-1(h)(2)(iii)). The file should include all medical records reviewed, internal notes, correspondence between reviewers, any surveillance reports, and the specific policy provisions relied upon.

2. Obtain Additional Medical Evidence: If possible, get updated physician statements and consider obtaining the following test(s) and information depending on your condition:

- A Functional Capacity Evaluation (FCE) to objectively measure your physical abilities

- Neuropsychological testing for cognitive or mental health conditions

- Updated imaging or diagnostic tests

- Detailed statements from all treating physicians addressing the denial reasons

- Vocational expert assessment of your ability to work

3. Address the Insurer’s Reasons for Denial: Carefully counter any arguments used against your claim.

4. Consult an ERISA Attorney: Legal guidance can improve your chances of success.

You must strictly meet all appeal deadlines. If you submit your appeal even one day late, you could lose benefits and forfeit your right to challenge the decision in court.

Related Article: Common Mistakes When Appealing a Denial of Long Term Disability BenefitsAfter the appeal is submitted, for disability claim appeals, it is supposed to be decided within 45 days, although the insurance company is allowed a 45-day extension it special circumstances exist, and notification is given before the 45 days expires. For disability claims, if the insurer or benefit administrator obtains evidence during the appeal that contradicts the claim, they must share this evidence and afford the claimant the opportunity to respond before they make their final decision.

Appeal Smarter, Not Later

Most people lose ERISA cases because their appeal file is too weak. Our free ‘Winning ERISA Claim Guide’ shows you exactly what to include—before it’s too late.

Download the Winning ERISA Claim Guide

What if the Appeal Is Denied?

If the insurer denies the appeal, the claimant’s next step is filing a lawsuit.

Court Jurisdiction and Trial Process

Because ERISA is a federal law, most ERISA benefit cases are heard in federal court. However, state courts may also have jurisdiction if both parties agree to keep the case there. Court rulings have determined that jury trials are not available in ERISA cases. ERISA litigation also differs from other types of lawsuits in key procedural ways.

Limitations in ERISA Litigation

Most courts impose strict limits on “discovery” in ERISA cases, restricting depositions and other forms of fact-gathering that typically occur in civil lawsuits. Instead, courts typically review only the evidence submitted during the claim and appeal process. As a result, verdicts are typically based exclusively on the claim record and legal submissions from both parties, with no live witness testimony, although the court may choose on its own to hear witness testimony.

The Standard of Review in ERISA Cases

One of the complexities of ERISA litigation is that even if a court finds an insurer’s decision incorrect, the claimant may still lose the case. This happens when the court applies the “abuse of discretion” or “arbitrary and capricious” standard of judicial review, which requires the claimant to prove the insurer’s decision was not just incorrect, but unreasonable. Whether this standard applies depends on the language in the insurance policy. If the policy grants the insurer or plan administrator “discretion” in decision-making, courts typically defer to the insurer’s judgment. This makes it especially important for claimants to be represented by attorneys experienced in ERISA litigation early in the appeal process so that they can develop the strongest possible arguments to counter or preempt potential legal hurdles.

Potential Outcomes of ERISA Litigation

If litigation is successful, courts may, but are not required to, award attorneys’ fees and prejudgment interest in addition to accrued benefits. However, fees are not recoverable at the claim appeal stage.

How to Strengthen an ERISA Appeal

- Obtain additional medical evidence: If the denial cited insufficient proof, consider obtaining a functional capacity evaluation (FCE) for certain physical illnesses, a neuropsychological evaluation if cognitive functioning is at issue, or a vocational assessment.

- Address policy interpretations: If the insurer relied on ambiguous policy language, counter it with legal arguments.

- Challenge insurer’s medical review: If the insurer used an independent medical examiner (IME), obtain a rebuttal from your treating physician, or another physician.

- Ensure procedural compliance: ERISA requires insurers to follow specific claims processing regulations. Identifying violations can strengthen your appeal.

How to Avoid Common ERISA Claim Mistakes and Strengthen Your Case

Filing an ERISA claim requires attention to detail, proper documentation, and strict adherence to deadlines. Many claimants unknowingly make errors that weaken their cases. In addition to the advice offered above, here are some additional critical steps to take and pitfalls to avoid ensuring the strongest possible claim.

Don’t Rely on Verbal Promises or Informal Communications

Insurance representatives may verbally suggest they will cover a claim, approve a treatment, or allow an extension—but if it’s not in writing, it doesn’t exist under ERISA. Keep copies of every communication, including emails and letters, and submit all evidence in writing.

Watch out for Surveillance and Social Media Pitfalls

Insurers frequently use video surveillance, social media monitoring, and online searches to find evidence that contradicts disability claims. A brief social media post or even casual outdoor activity can be misrepresented as proof of ability to work.

Don’t Appeal Without Strengthening Your Case

Simply resubmitting the same claim with a letter stating “I disagree” is not enough. An appeal should correct deficiencies in the original claim, such as:

- Providing additional medical records or physician statements.

- Obtaining a vocational expert’s evaluation of your ability to work.

- Addressing insurer arguments with new supporting evidence.

Consider Legal Assistance Early

Many ERISA claimants wait until after a final denial to seek legal help, which can be a mistake. Courts rarely allow new evidence once a case moves to litigation. Working with an ERISA attorney during the appeal stage can increase the chances of success before going to court.

Final Thoughts

ERISA claims involve strict deadlines and complex legal standards. Successfully challenging a denial requires thorough preparation and strong supporting evidence.

The pre-litigation claim appeal is your only opportunity to build the complete record that a court will review. Recent federal court decisions emphasize that insurers must engage in a “meaningful dialogue” with claimants and properly consider treating physician opinions. With insurance companies continuing to prioritize profits over patient care, having experienced legal representation has become increasingly important for protecting your rights.

If your claim has been denied or if you need guidance before filing, working with an experienced ERISA attorney can make the difference. Contact DeBofsky Law to discuss your case and protect your benefits.

Frequently Asked Questions About Winning ERISA Claims

What should I do if the insurance company keeps requesting more information?

Insurance companies may sometimes delay claims by continuously requesting additional documentation and may even request information again that has already been submitted. If that occurs, politely comply but firmly emphasize that the documentation was previously submitted and attach evidence of transmittal. Claimants should also firmly request that they receive a timely determination in accordance with the deadlines set forth in the U.S. Department of Labor’s ERISA Claim Regulations.

How does an ERISA appeal differ from a new claim submission?

An ERISA appeal is not just a resubmission of the same claim. It is a legal challenge that must specifically address the reasons for denial and provide additional evidence in support of the claim. If the denial was based on a policy interpretation, the appeal must counter it with legal arguments. Importantly, the appeal is often the final opportunity to introduce new evidence. If the case later goes to court, the judge typically only considers what was submitted during the appeal.

Does my employer control my ERISA benefits, or does the insurance company?

It depends on how the plan is structured. If the plan is fully insured, the insurance company both administers the claims and pays benefits, meaning the employer has no financial stake in approvals or denials. However, if the plan is self-funded, the employer directly pays claims, which can create a financial conflict of interest. In self-funded plans, even if an insurance company administers the claims, the employer has the final say in approving or denying benefits.

Can my benefits still be terminated after winning an appeal?

Yes. Winning an ERISA appeal does not guarantee future payment of benefits indefinitely. Insurers frequently monitor claimants for potential termination by:

- Requiring updated medical reviews or independent medical exams.

- Conducting video surveillance to dispute physical limitations.

- Examining social media to see if any postings contradict claimed limitations

- Claiming medical improvement based on minor inconsistencies in doctor reports.

What if my claim is delayed instead of denied?

Insurance companies sometimes delay claims instead of outright denying them. ERISA regulations require claims to be decided within specific timeframes, but insurers may request excessive information, repeatedly ask for documents already submitted, or take other steps to stall the process. These tactics can be frustrating and may financially harm claimants.

- You have the right to demand a timely decision under ERISA rules.

- If delays persist, you may need to escalate your case or consider initiating legal action.

- Learn more about when you can sue for delays.

To protect against termination, claimants should continue medical treatment, keep detailed records of symptoms, and document any work-related restrictions over time.