Disability insurance claim denials have been increasing in 2024. While the reasons are not entirely clear, the uptick in denials is apparent. We have identified several recurrent issues that are cited by disability insurers as the basis for claim denials. Understanding why disability claims are denied is crucial for claimants seeking to avoid common pitfalls and secure the benefits they deserve. We present this guide to help prospective disability claimants avoid pitfalls when they submit their claims. We also offer suggestions on how claimants, with the assistance of a knowledgeable and experienced attorney, may be able to overcome an unjustified denials.

This comprehensive guide examines the ten most common reasons insurance companies deny disability claims, from failure to meet policy definitions and insufficient medical evidence to surveillance tactics and biased medical examinations. We explain the three major hurdles every claimant must overcome, provide specific strategies to strengthen your claim at each stage, and outline your options if your claim is denied, including when and why you need an experienced ERISA attorney.

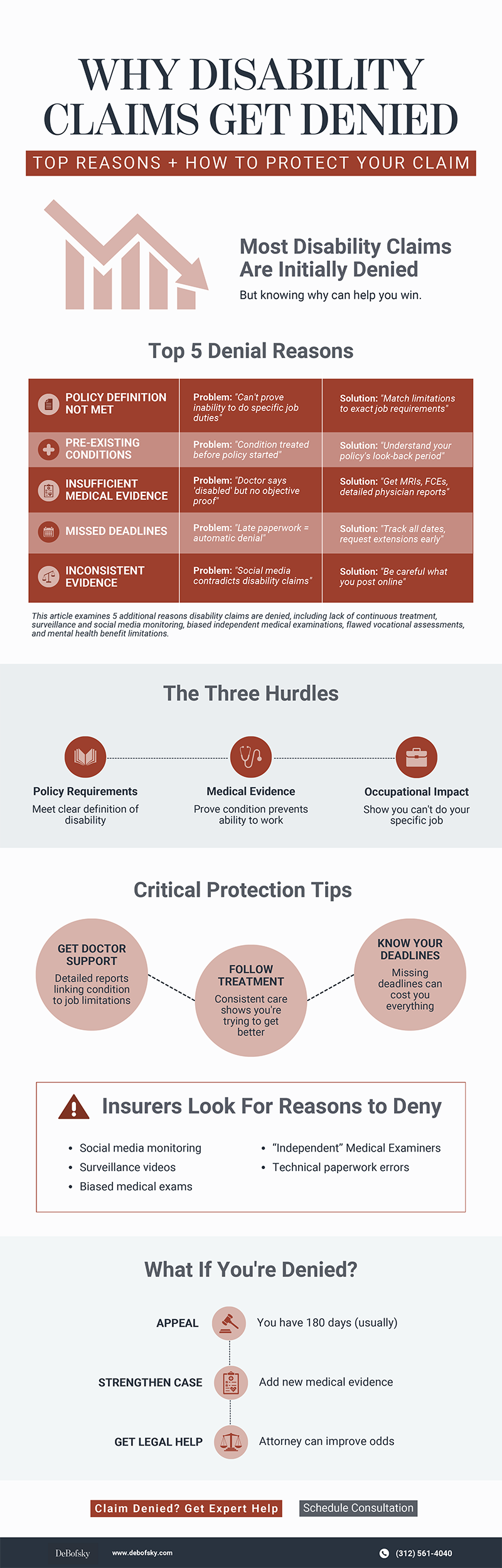

Three Major Challenges to Qualify for Disability Insurance Benefits

Disability insurance is a unique type of coverage that requires claimants to overcome three major hurdles to qualify for benefits:

- Meeting Policy Requirements: Claimants must satisfy the policy’s definition of disability and avoid exclusions, such as pre-existing conditions or procedural errors.

- Providing Sufficient Medical Evidence: Claimants need to demonstrate how their condition causes restrictions and limitations that interfere with their ability to work.

- Establishing Occupational Impact: Medical restrictions must align with an inability to perform the essential duties of their current job or employment in general.

A doctor’s statement that their patient is “disabled” is usually not sufficient for a claimant to qualify for benefits. As a result, a claimant needs to back-up a physician’s certification of disability with additional evidence such as laboratory test findings, radiologic imaging, or other types of objective testing.

Most Common Reasons Why Disability Insurance Claims Are Denied & What You Can Do About Them

Below, we explore some of the most frequent reasons why disability claims are denied and how claimants can strengthen their cases.

1. Failure to Meet Policy Definitions

Disability insurance policies contain specific definitions of what constitutes a disability, which vary significantly. Some policies define disability as the inability to perform the duties of your own occupation (called an “own occupation” definition). Others use a broader definition, requiring claimants to prove they cannot perform any occupation for which they are qualified (called an “any occupation” definition).

For example, a surgeon who develops hand tremors may be unable to perform surgery but could potentially work in medical consulting or teaching. Under an “own occupation” policy, this surgeon would qualify as disabled. Under an “any occupation” policy, the insurer could argue the surgeon is not disabled because other medical work exists.

Even with an occupational definition of disability, claims may be denied if the claimant works part-time, takes another job, or owns a business that continues to generate profits, which may lead insurers to argue that the claimant does not meet the policy’s definition of disability. Additionally, the definition of “disability” in many policies may transition from an “own occupation” standard to an “any occupation” standard after 24 months, making it more difficult to qualify. At that stage, claimants must show they cannot perform even sedentary or alternative work that would meet a certain wage threshold.

In evaluating whether claimants meet these definitions, insurers must consider factors such as education, training, and previous employment. For example, in Erreca v. W. States Life Ins. Co., 19 Cal. 2d 388, 394 (Cal. 1942), the court held that insurers cannot deny benefits by claiming a professional worker with substantial earnings can perform low-wage jobs. Similarly, claimants with only a high school diploma and no relevant work experience cannot be denied benefits based on their ability to perform jobs requiring advanced training or education.

Protect your claim:

- Understand your policy’s definition of disability, including any transition periods (e.g., from “own occupation” to “any occupation”). Tailor your documentation to address these standards.

- Include specific evidence that demonstrates why you cannot perform your job duties or any other occupation, based on your education, training, and experience.

- Provide examples of activities (including everyday activities) you cannot perform to show how your condition prevents you from meeting job requirements.

2. Pre-Existing or Other Disqualifying Conditions

Unlike health insurance, which under the Affordable Care Act prohibits pre-existing condition exclusions, disability insurance policies often deny benefits if the disabling condition was diagnosed or treated, and in some instances, even suspected before the policy’s effective date. Group disability insurance policies typically include a “look-back” period, ranging from three to six months before coverage begins, during which insurers investigate whether the claimant received treatment or prescriptions for the condition. If the condition falls within this period, the claim may be denied, regardless of the severity of the impairment. For example, if you received treatment for back pain in March 2024 and your group disability coverage began June 1, 2024, a policy with a three-month look-back period would exclude coverage for that back condition.

For short-term disability (STD) policies, pre-existing condition exclusions are less common, meaning you may still qualify for STD benefits even if you are ineligible for long-term disability (LTD) benefits. Individual disability insurance policies, on the other hand, often include “incontestability” provisions. These provisions allow insurers to revoke coverage due to factual omissions or misstatements on the application, but typically only within the first two years after the policy is issued.

Disqualifying conditions extend beyond pre-existing conditions. Disability insurance policies often exclude coverage for injuries or illnesses incurred while committing a crime. Some courts have even ruled that injuries sustained while driving under the influence of alcohol or drugs fall into this category. Disabilities caused by self-inflicted injuries are also excluded.

Protect Your Claim:

Related Article: How to Defeat a Pre-Existing Condition Exclusion Denial

- Review your policy to understand its look-back period, disqualifying conditions, and incontestability provisions.

- Work with your doctor to document when your condition began and whether it predates the policy’s effective date.

- Consult with an experienced disability benefits attorney to challenge denials related to pre-existing conditions, criminal exclusions, or alleged misstatements.

3. Insufficient Medical Evidence

A lack of sufficient medical evidence is one of the most common reasons disability insurance claims are denied. Insurers often require objective test results, such as x-rays, MRIs, electrodiagnostic tests, lab findings, or psychological testing, to support a disability claim. Without these results, claims are frequently denied, especially for behavioral health conditions. Denials can also occur if treatment records are incomplete, clinical findings are missing, or there are inconsistencies between the severity of the claimed condition and the level of treatment provided.

What qualifies as objective evidence? Objective evidence includes measurable medical data: MRI or CT scans showing structural damage, laboratory blood work results, electrodiagnostic testing (EMG, nerve conduction studies), pulmonary function test scores, or neuropsychological testing results.

What about subjective symptoms? Subjective symptoms—your reports of pain levels, fatigue, dizziness, or how you feel—are legitimate but insufficient alone. Insurers require your physician to connect these symptoms to objective test findings and document specific functional limitations.

Disabilities involving subjective symptoms, such as pain, fatigue, or dizziness, pose additional challenges. These conditions often lack measurable data, and insurers may dismiss claims unless supported by tools like functional capacity evaluations or neuropsychological testing. Episodic conditions, which may include auto-immune disorders such as rheumatoid or psoriatic arthritis, or migraine headaches, to name examples, complicate matters further because symptom severity can fluctuate, allowing claimants to experience “good days” along with bad days.

Strengthen your claim:

- Ensure your treating doctor provides detailed documentation of specific limitations, such as difficulties standing, lifting, or concentrating, and ties them directly to your job tasks. Physicians should not simply state that a patient is “unable to work.” Instead, they need to describe specific limitations, such as difficulties sitting, standing, lifting, or concentrating and explain the rationale for such limitations.

- Use objective evidence, such as MRIs, functional capacity evaluations, or psychological testing, to support your claim. Where possible, doctors should include objective data and explain how these restrictions prevent the claimant from performing job-related tasks.

- Include records explaining the episodic nature of your condition if symptoms fluctuate. This may take the form of regularly kept symptom diaries or logs.

4. Lack of Continuous and Appropriate Treatment

Disability insurance policies often require claimants to follow a consistent and appropriate treatment plan to qualify for benefits. While insurers generally cannot force claimants to undergo surgery or other invasive procedures as a condition of receiving benefits, they may deny claims if treatment appears sporadic or inadequate. For example, treatment by non-specialists for complex conditions or failure to take prescribed medications that have proven effective can result in a denial. Missing appointments or ignoring follow-up recommendations from doctors can also raise red flags.

To avoid treatment-related denials, claimants should:

- Follow all treatment recommendations, including attending appointments and taking prescribed medications.

- If seeing a specialist is necessary, schedule appointments as soon as possible and document efforts to comply with their recommendations.

- Keep detailed records of your treatment history, even if you experience gaps in care due to financial or logistical challenges.

By demonstrating that you are committed to managing your condition, you can strengthen your claim and reduce the likelihood of denial.

5. Missed Deadlines and Incomplete Forms

The paperwork required for disability insurance claims is often tedious, but failing to meet deadlines or submit necessary forms can lead to a denial. Insurers typically require documentation such as proof of loss, earnings records, and authorization forms allowing them to gather medical and vocational information. Missing deadlines for producing such evidence can result in delays or outright denials.

Many policies include strict timelines for submitting proof of loss, often requiring forms within 30 to 90 days, and no later than one year from the onset of disability. Some states apply the notice-prejudice rule. That insurance law doctrine requires insurers to prove they were harmed by a late submission before denying a claim. However, other states, like Illinois, enforce stricter deadlines, and these rules do not apply to self-funded plans.

Key Deadlines to Track:

- Proof of Loss: Typically due within 30-90 days of disability onset; no later than one year

- Appeal Deadline (ERISA): Usually 180 days from denial letter (some policies allow only 60 days)

- Second Appeal: Some policies allow an additional appeal; check your specific plan

Missing any of these deadlines can permanently bar your claim.

Claimants who miss deadlines due to circumstances such as mental incapacity (e.g., depression) may still be able to argue for leniency with sufficient documentation. Insurers may also grant deadline extensions upon request. However, it’s crucial to communicate promptly and provide any requested information as soon as possible.

To avoid these issues:

- Create a checklist or calendar specifically for all submission deadlines outlined in your policy.

- Double-check all forms to ensure accuracy and completeness. Attach all requested documentation to avoid delays.

- If you anticipate missing a deadline, notify the insurer immediately and request an extension in writing.

Understanding your policy’s specific deadlines and compliance requirements is essential to ensuring your claim is not denied for technical reasons.

6. Discrepancies in the Evidence

Insurance companies closely scrutinize every piece of information they collect, searching for inconsistencies in the claimant’s statements, medical records, or activity reports. Any discrepancy between what a claimant reports and what the medical evidence shows can become the basis for a denial. For example, if a claimant states they cannot leave their home, but is observed running errands or engaging in strenuous activity, insurers may cite this as evidence to deny benefits.

Claimants must be honest and forthright when reporting symptoms. Exaggerating or embellishing symptoms not only weakens the claim but can damage credibility with the insurer. Even minor inconsistencies, such as failing to update medical records to reflect changes in treatment, can raise red flags.

To strengthen your claim:

- Review all submitted information to ensure it aligns with your medical records and reported symptoms.

- If discrepancies arise (e.g., inconsistent statements or conflicting records), address them promptly with updated documentation or clarification from your doctor.

- Be transparent about symptom variability, noting any fluctuations in severity or duration.

7. Surveillance and Social Media Activity

Yes, disability insurers regularly review claimants’ social media accounts and may hire investigators to conduct video surveillance. Although not every claim involves surveillance, insurers use it strategically when they suspect inconsistencies.

Insurance companies are also increasingly scrutinizing social media posts for inconsistencies. Claimants should avoid posting anything that could be taken out of context, such as photos or videos of physical activities that insurers might use to question their disability. They should also never list fictitious jobs on platforms like LinkedIn to fill resume gaps, as this can severely harm credibility. Additionally, it’s wise to ask friends not to “tag” you in posts that could misrepresent your condition.

To protect your claim:

- Be mindful of the content you post online and its potential to be misinterpreted.

- Regularly review privacy settings on social media platforms.

- Consider explaining social media posts to your attorney if you believe they might be misconstrued by an insurer.

- Staying cautious with social media posting and online activities and avoiding potentially misleading activities can help protect your claim from unfair denials.

8. Independent Medical Examinations (IMEs)

On occasion, disability insurance companies may require claimants to undergo what is misnamed as an Independent Medical Examination (IMEs). These exams are not truly independent, as the insurer selects the doctor—often someone who has provided favorable reports for the insurer in other cases. While claimants must cooperate with these requests, they should also prepare for potential examiner bias. The examiner may be hostile or dismissive of the claimant’s condition, and their report could result in a denial.

Refusing an examination request is considered a lack of cooperation and will almost always lead to a claim denial.

To protect your claim:

- Approach the IME professionally and answer questions honestly but succinctly.

- Keep a record of the exam, including the examiner’s questions, behavior, and the duration.

- Consult an attorney if you suspect the examiner’s report may be biased or incomplete.

9. Vocational Assessments

Disability insurance companies rely on vocational assessments performed by vocational rehabilitation consultants who clarify a claimant’s job duties and may determine whether the medical findings support the claimant’s ability to perform their usual job or other jobs. It is critical for claimants to make sure the insurance company is provided with an accurate and detailed description of their job, or the critical duties of their occupation may not be considered, which could lead to a denial.

Protect Your Claim:

- Provide a detailed job description, highlighting critical duties and physical or cognitive requirements.

- If the insurer’s vocational assessment is inaccurate, request clarification or provide additional evidence to correct errors.

- Work with an attorney to challenge any vocational findings that misrepresent your job duties or employability.

10. Limited-Duration Benefits for Mental and Subjective Conditions

Many disability insurance policies impose strict limitations on benefits for mental health conditions and so-called “subjective” conditions, such as chronic fatigue syndrome or fibromyalgia. These policies often cap benefits at two years, even if the claimant remains totally disabled. Similarly, neuromusculoskeletal and soft tissue disorders, which are often characterized by pain or limited mobility, may also fall under these limited-duration provisions.

To continue receiving benefits beyond the two-year mark, claimants must demonstrate that their disability stems from a condition not subject to the policy’s limitations. This can be particularly challenging if the plan administrator attributes the disability entirely or partially to a capped condition. However, the burden of proving that policy limitations apply rests with the plan administrator.

Claimants facing these limitations should:

- Provide Comprehensive Medical Evidence: Work closely with medical providers to establish that the primary disabling condition is not subject to the policy’s limitations.

- Request Detailed Rationale for Denials: Ensure that the plan administrator explains why the condition is considered limited-duration.

- Seek Legal Guidance: Consult with an attorney to challenge improper application of policy caps and develop a strong case for continued benefits.

Can You Appeal Disability Insurance Claim Denial?

Disability insurance plans fall into two categories: ERISA-governed plans (typically employer-provided) and non-ERISA plans (such as individual or certain government or religiously based employers’ plans). ERISA plans are subject to strict rules, including requirements for pre-suit appeals and limitations on introducing new evidence in litigation. Non-ERISA plans may follow different rules. Understanding whether your plan is ERISA or non-ERISA is crucial for protecting your rights during the claim process.

If your disability claim is denied, you have the right to appeal. In fact, if your disability claim is subject to the federal ERISA statute, you almost always must appeal the denial in a timely manner, since failure to do so could later bar you from filing suit. Under ERISA, your disability plan administrator is required to notify you of an adverse benefit determination in writing and provide you with at least 180 days to appeal (or, in some cases, as little as 60 days). You have the right to request a copy of your claim file and the underlying plan documents.

Even if your claim is not subject to the federal ERISA statute (for instance, because it’s through a governmental or church plan, payroll practice, or individual policy of insurance), you may still have the right to appeal. You should consult the denial letter and policy or plan document to confirm. Alternatively, you may proceed directly to court.

What Happens if a Disability Insurance Appeal to Fails?

If an appeal fails, claimants may have options such as filing a lawsuit, negotiating with the insurer, or exploring alternative dispute resolution methods like mediation. Taking action quickly is critical, as strict time limits apply. For more details, see our blog on “All the Things that Can Go Wrong in an Appeal.”

Let’s Get You Results – Get in Touch for a Confidential Consultation

Do You Need an Attorney to Appeal a Disability Denial?

The most common question claimants ask is when to hire an attorney—should you handle the initial claim yourself and only hire an attorney if denied? For ERISA disability claims, waiting until after your appeal is denied is usually too late. Because courts limit review to evidence submitted during your administrative appeal, your appeal is effectively your only trial. Hiring an attorney before filing your appeal gives you the best chance of success.

There is no requirement that you hire an attorney to assist with appealing a disability claim denial. However, it is generally not wise to attempt to appeal on your own. An experienced disability claim attorney can significantly improve your chances of success during the appeals process and in any litigation that follows. For claims governed by ERISA, the law often limits what can be added to the claim file during litigation. Therefore, it is critical to build a complete claim file during the pre-suit appeal process.

An experienced attorney will request your claim file and plan document to verify that the plan language cited in the denial letter is accurate. The attorney can also identify any additional evidence needed to strengthen your claim. They may recommend neuropsychological evaluations, functional capacity assessments, or other tests to support your case. Additionally, they might request your doctors to provide specific information to clarify your condition and limitations.

During the appeals process, the attorney ensures that all evidence supporting your case is addressed. If the insurer introduces new evidence, the attorney responds directly, giving you the final word before a decision is made. If the appeal is denied, an attorney who handles litigation can transition your case to court and help maximize your recovery.

How Long Will It Take to Appeal a Denial of Disability Benefits?

Disability claimants with ERISA-governed plans are typically given 180 days to appeal a denial. After submitting the appeal, the plan administrator has 45 days to make a decision. If “special circumstances” arise, the administrator can extend the deadline by an additional 45 days, provided they notify the claimant before the initial review period ends.

Under 29 CFR § 2560.503-1(f)(4), the ERISA claims regulations permit the insurance company to defer rendering a decision (known as “tolling” of the appeal deadline), but only if the claimant fails to provide necessary information for the appeal. For example, the insurer or plan administrator may pause the timeline to gather medical records on your behalf. However, the administrator cannot toll the deadline to obtain evidence for which they are responsible, such as a vocational report or an internal medical review. Please review our ‘how long it takes to appeal a claim denial‘ article to learn more.

Can You Be Denied Disability Benefits Again After Successfully Appealing?

Unfortunately, disability plan administrators can deny a claim multiple times, with no legal limit. For example, you might successfully appeal an initial denial, only to face another denial two years later due to a change in the definition of “disability.” Insurers generally avoid frivolous denials because they reflect poorly in court. However, ERISA’s lack of compensatory and punitive damages removes deterrence against bad faith claim denials.

In non-ERISA plans, repeated denials could qualify as an unfair or deceptive claims practice. Such actions may expose the insurer to bad faith liability.

Takeaway: Tips for Avoiding Disability Claim Denials

To strengthen your claim and minimize the risk of denial:

- Organize Your Documentation: Submit up-to-date and detailed medical records, test results, and prescription information that clearly explain your disabling condition.

- Know Your Policy: Understand your policy’s terms, exclusions, and requirements before filing a claim.

- Get Physician Support: Ensure your treating doctor fully supports your claim with detailed and consistent medical evidence.

- Follow Treatment Plans: Adhere to your doctor’s recommendations, attend regular appointments, and take prescribed medications.

- Communicate Honestly: Be polite, accurate, and transparent when speaking with the insurer. Avoid exaggerating or downplaying symptoms.

- Meet Deadlines: Submit requested documents on time. If delays arise, notify the insurer and request an extension.

- Seek Professional Help: Early guidance from an experienced disability attorney can help avoid costly mistakes. If your claim is denied, consult a professional immediately to navigate the appeals process effectively.

Quick Reference: Why Disability Claims Get Denied Visual Guide

This article examines 5 additional reasons disability claims are denied, including lack of continuous treatment, surveillance and social media monitoring, biased independent medical examinations, flawed vocational assessments, and mental health benefit limitations.

Conclusion

Due to the complexity of disability claims, even if a claim is well-supported by clinical findings and medical test results, it may still be denied. If that occurs, claimants need to turn to a knowledgeable and experienced professional for assistance in challenging an unwarranted claim denial. The attorneys at DeBofsky Law have the experience, knowledge, and tenacity to provide claimants with the assistance they need during the claim process, for appeals, or in court.