Group disability insurance offers financial protection by providing income replacement when an individual cannot work due to illness or injury. Yet navigating these policies can be complex, particularly due to the often-included pre-existing condition exclusions. These exclusions limit coverage for conditions that existed before the policy’s effective date, frequently leading to unforeseen hurdles and claim denials. This article demystifies the nuances of pre-existing condition exclusions in disability claims, providing essential knowledge and guidance to navigate these challenges effectively.

What Are Pre-Existing Conditions?

A pre-existing condition refers to any health issue, injury, or illness an individual has before obtaining insurance coverage. The goal of pre-existing condition policy exclusions is to prevent individuals from securing coverage after discovering or anticipating a condition that could result in a disability claim.

However, having a past medical diagnosis does not automatically mean your current disability is pre-existing. The exclusion only applies under specific circumstances defined by your policy.

How Pre-Existing Condition Exclusions Work

Pre-existing condition exclusions serve as a means for insurance companies to manage risk. They help prevent adverse selection, where individuals might obtain coverage knowing they have an imminent risk of disability due to a pre-existing condition.

These exclusions typically restrict coverage for a specified period after the policy’s effective date. During this period, the policy might not cover disabilities caused by pre-existing conditions. However, once this waiting period elapses, coverage for pre-existing conditions could begin.

Three Key Elements That Define Pre-Existing Conditions

Most disability policies define a pre-existing condition using three key elements:

- The Lookback Period: A window of time (typically 3 to 6 months) before your coverage started during which the insurer examines your medical history.

- Treatment, Diagnosis, or Symptoms: Whether you received medical care, were diagnosed, or experienced symptoms during the lookback period.

- The Filing Window: How long after coverage begins you can file a claim before the exclusion no longer applies (usually 12 to 24 months).

For instance: Coverage starts January 1, 2024, with a 3-month lookback period. The insurer reviews October 1 through December 31, 2023. If you file a disability claim before January 1, 2025, they can invoke the exclusion if they find relevant treatment during the lookback period. If you file after January 1, 2025, the exclusion cannot be applied.

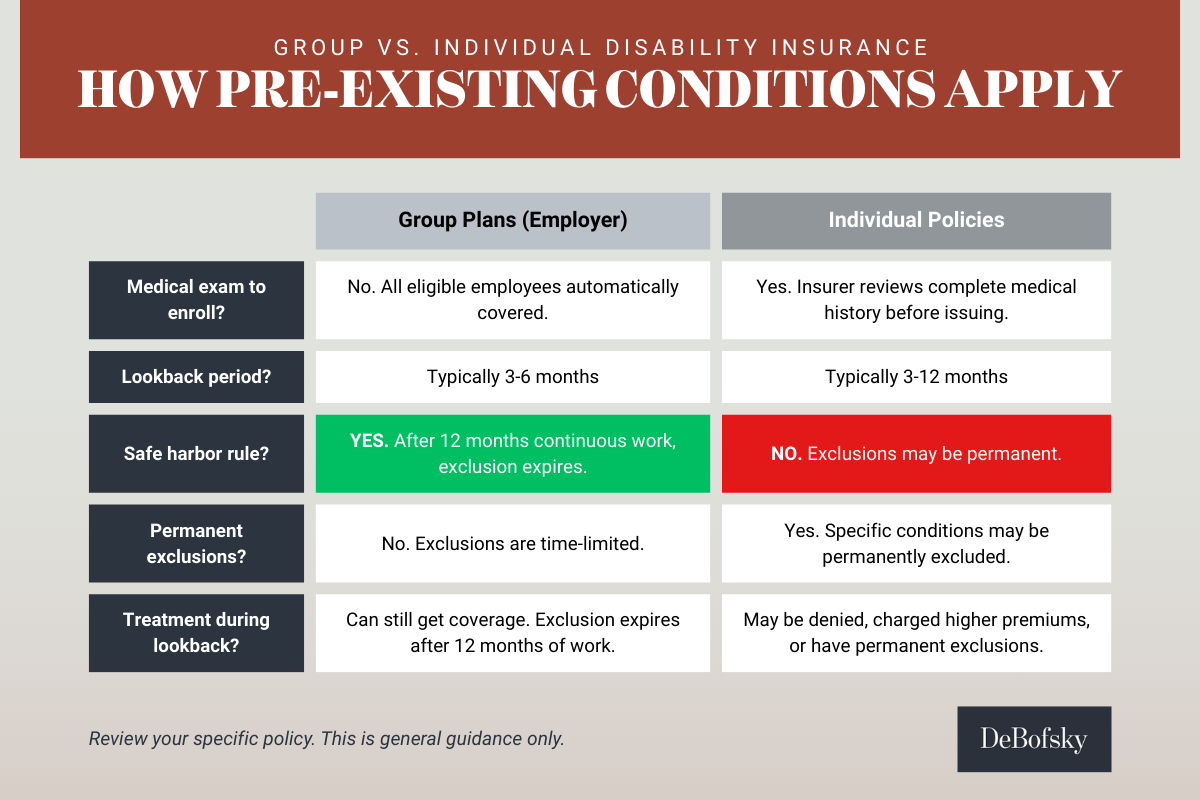

Group Plans vs. Individual Policies: Critical Differences

Understanding whether you have a group disability plan (through your employer) or an individual policy (purchased directly) is crucial. They handle pre-existing conditions very differently.

Group or Employer-Sponsored Plans

The 12-Month Safe Harbor Rule:

For group plans, once you have worked for your employer for a full year without filing a disability claim, the pre-existing condition exclusion typically expires. This applies even if you had treatment during the lookback period. This critical protection is unknown to many claimants.

Key Features:

- No medical underwriting when you enroll (insurer does not review your health history upfront)

- Lookback period: Usually 3 to 6 months

- Filing window: Typically 12 months

- After 12 months of active work: Pre-existing exclusion no longer applies

Consider this scenario: You started your job on January 1, 2024, with immediate group LTD coverage. You were treating a chronic condition during the lookback period. If you become disabled and file a claim in February 2024, the insurer can invoke the exclusion. But if you continue working until February 2025 and then become disabled, the exclusion no longer applies.

Individual Disability Policies

Medical Underwriting at Purchase:

When you buy an individual policy, the insurer reviews your complete medical history upfront and may:

- Permanently exclude specific conditions from coverage

- Charge higher premiums due to your health status

- Add waiting periods for certain conditions

- Deny coverage entirely

Key Differences:

- Pre-existing exclusions may be permanent (not time-limited)

- You must accurately disclose all medical history on application

- Exclusions are negotiated and written into your specific policy

- No “safe harbor” period (exclusions last as long as policy states)

Bottom Line: If you have a group plan and can continue working for 12 months, you may avoid the pre-existing exclusion entirely. If you have an individual policy, review your specific exclusions carefully because they may be permanent.

Ambiguity in Pre-Existing Condition Exclusion Language

One major point of contention in legal cases involving pre-existing condition exclusions is the ambiguity of the policy language. If the exclusion’s wording is vague or open to interpretation, courts tend to favor the insured party. Ambiguous language could result in a broader interpretation of coverage, potentially favoring the insured’s claim.

Under insurance law, ambiguous policy language must be interpreted in favor of the policyholder, not the insurance company. If your policy’s pre-existing condition exclusion is unclear about what constitutes “treatment,” “diagnosis,” or the lookback period, courts will resolve that uncertainty in your favor.

Examples of ambiguous language:

- Does “treatment” include over-the-counter medications?

- Does “consulted a physician” include telemedicine visits?

- Does “symptoms” require a formal diagnosis, or just discomfort?

If your denial letter relies on vague policy language to justify the exclusion, this creates a strong basis for appeal.

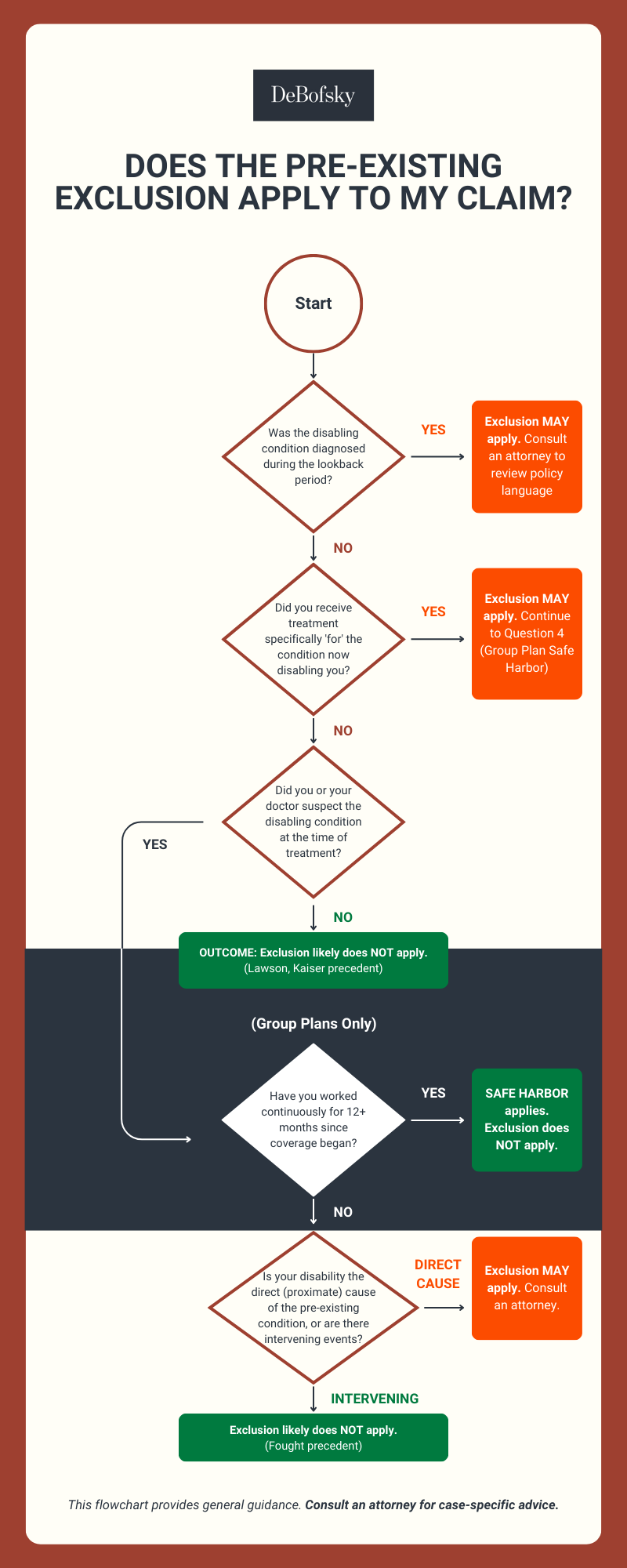

Pre-Existing Condition Must Be Known or Suspected

Disability insurers sometimes stretch the language of a pre-existing condition exclusion to encompass treatment for conditions that were neither diagnosed nor suspected during the lookback period.

Case Example: Cancer Misdiagnosed as Respiratory Infection

In Lawson v. Fortis, 301 F.3d 159 (3d Cir. 2002), the insurer denied coverage for the claimant’s cancer diagnosis because she received treatment during the lookback period for a respiratory infection that later proved related to cancer. The Third Circuit Court of Appeals ruled that the insurer abused its discretion. The court held that a patient cannot receive treatment “for” a condition that is neither diagnosed nor expected, particularly when the treatment offered was wrong for the actual condition.

Case Example: Routine Screening Is Not Treatment

In Pitcher v. Principal Mutual Life Ins. Co., 93 F.3d 407 (7th Cir. 1996), the Seventh Circuit ruled that an insurer abused its discretion when it denied disability benefits to a breast cancer patient who underwent a mammogram during the lookback period. The court observed that the mammogram was not “for” breast cancer but rather for monitoring her longstanding fibrocystic breast condition. The court further noted that mammograms are not “treatment” but rather diagnostic procedures.

The Legal Standard: Treatment Must Be “For” the Disabling Condition

Courts have consistently held that for a pre-existing condition exclusion to apply, you must have received treatment specifically “for” the condition that is now disabling you. Treatment that, in hindsight, turned out to be related does not qualify.

This principle protects you when:

- You saw a doctor for non-specific symptoms later diagnosed as something else

- You underwent routine screening or monitoring (not active treatment)

- You received treatment for a misdiagnosed condition during the lookback period

- The actual disabling condition was not suspected by you or your doctor at the time

Case Example: When the Condition Was Not Suspected

In Kaiser v. United of Omaha, 2016 WL 379814 (W.D. Wis. 2016), an employee saw her doctor for shoulder pain during the lookback period. The doctor diagnosed tendinitis (believed to be from shoveling snow) and prescribed anti-inflammatory medication. Months later, testing revealed lung cancer causing the pain.

The insurer denied the claim, arguing the doctor visit was treatment “for” cancer. The court rejected this and established an important test: “There at least must have been some concern or suspicion at that time that the observed symptoms were caused by the particular condition in order for the patient to be considered as being treated or seen for the particular condition.”

In other words: If neither you nor your doctor suspected the disabling condition during the lookback period, you were not receiving treatment “for” that condition, even if the symptoms were ultimately caused by it.

Proximate Causation Required

Disability insurers may not interpret the pre-existing condition exclusion so broadly as to encompass complications resulting from a pre-existing condition.

In Fought v. UNUM Life Ins. Co., 379 F.3d 997 (10th Cir. 2004), the insurer denied coverage for disability due to a staph infection that resulted from elective heart surgery the claimant underwent during the lookback period. The Tenth Circuit ruled that the decision was an abuse of discretion because it relied on classic but-for causation when proximate causation is required.

Understanding But-For vs. Proximate Causation:

Insurance companies often try to create a chain of causation to deny claims: “But for your pre-existing heart condition, you would not have needed surgery, would not have gotten an infection, and would not be disabled.”

Courts reject this approach. The legal standard is proximate causation. The pre-existing condition must be the direct cause of your disability, not merely part of a chain of events.

The Fought court explained: “For Ms. Fought, there were at least five intervening stages between the pre-existing coronary artery disease and the disability: The failure of non-surgical alternatives, initially successful elective surgery, later complications from that surgery, initially successful treatment of those complications, and finally a drug-resistant infection. UNUM seems to suggest that it need not cover anything for which it can construct a but-for story. If we were to accept this contention, we would effectively render meaningless the notion of the pre-existing condition clause by distending the breadth of the exclusion.”

Additional examples where proximate causation protects claimants:

- Pre-existing diabetes, surgical complication, disabling infection (the infection is not pre-existing)

- Pre-existing lower back pain, new disc herniation at different spinal level, disability (the new herniation is not pre-existing)

- Pre-existing hypertension treatment, stroke, disability (cannot use risk factor as proxy for stroke)

Insurers cannot stretch a causal chain indefinitely to deny your claim. If there are intervening events, complications, or new conditions between your pre-existing condition and your disability, the exclusion likely does not apply.

Curious if Pre-Existing Exclusion Applies to your Case? Learn from our infographic.

Common Insurer Tactics: How They Misapply Pre-Existing Exclusions

Insurance companies routinely overreach when applying pre-existing condition exclusions. Recognizing these tactics can help you identify wrongful denials.

Tactic 1: Connecting Unrelated Symptoms

The tactic: Insurers review your medical records and find any complaint during the lookback period, then claim it relates to your current disability, even when your doctors never made that connection.

A common scenario: You are disabled by severe migraines. During the lookback period, you saw your doctor for occasional tension headaches. The insurer claims “headaches are headaches” and denies your claim. However, tension headaches and migraines are medically distinct conditions.

Your response: Obtain a letter from your treating physician explaining the medical distinction between the symptom during the lookback period and your current disabling condition.

Tactic 2: The “Reasonable Person Would Have Known” Argument

The tactic: Even if you never saw a doctor during the lookback period, insurers argue you should have because a “reasonable person” would have recognized the symptoms.

A common scenario: You had occasional back discomfort during the lookback period managed with over-the-counter pain relievers. Four months after coverage began, you developed severe sciatica requiring surgery. The insurer argues you “should have known” to see a doctor.

Your response: Emphasize that you experienced only minor, non-specific symptoms that did not warrant medical attention. Many people have occasional aches without seeking care.

Tactic 3: Treating Risk Factors as Pre-Existing Conditions

The tactic: Insurers conflate risk factors or preventive treatment with actual disabling conditions.

In Meyer v. Unum Life Insurance Co., 2015 WL 1470447 (D. Kan. 2015), a banker became disabled after a stroke. Before coverage began, he was treated for atrial fibrillation and hypertension, both risk factors for stroke. Unum denied his claim, arguing treatment for these risk factors meant he was being treated “for” stroke.

The court rejected this: “Unum could not lawfully treat risk factors as proxies for pre-existing conditions.”

Additional examples of risk factor overreach:

- High cholesterol treatment is not heart disease

- Blood pressure medication is not congestive heart failure

- Diabetes monitoring is not diabetic neuropathy

Your response: Point out the legal distinction between preventive care for a risk factor and treatment for the actual disabling condition. The Meyer decision establishes that insurers cannot make this argument.

Tactic 4: Using Post-Lookback Medical Records Against You

The tactic: Insurers review medical records created after the lookback period and cherry-pick statements to suggest your condition existed earlier.

A common scenario: You became disabled 4 months after coverage began. You told your doctor, “I have been experiencing symptoms for about 6 months.” The insurer uses this statement to argue you had symptoms during the lookback period, even though you never sought treatment then.

Your response: Emphasize that the relevant question is whether you were treated for, diagnosed with, or consulted a physician about the condition during the lookback period, not whether you later recalled vague symptoms.

Tactic 5: Claiming Diagnostic Procedures Are “Treatment”

The tactic: Insurers argue that diagnostic testing (X-rays, MRIs, mammograms) during the lookback period constitutes “treatment.”

The Pitcher case addressed this directly. A routine mammogram for monitoring fibrocystic breast condition was not “treatment for” breast cancer diagnosed later. The court noted that diagnostic procedures are not “treatment.”

Your response: Distinguish between diagnostic procedures (tests that identify or monitor conditions) and treatment (medical interventions that address a diagnosed condition). Courts consistently hold that routine screening is not “treatment.”

Understanding Critical Time Periods

One of the biggest sources of confusion involves the various time periods in disability policies.

Lookback Period

Definition: The window of time before your coverage started during which the insurer examines your medical history.

Typical duration: 3 to 6 months (can be up to 12 months for individual policies)

For instance: Coverage starts January 1, 2024. With a 3-month lookback, the insurer reviews October 1 through December 31, 2023.

Filing Window (Pre-Existing Condition Application Period)

Definition: How long after coverage begins the insurer can apply the pre-existing exclusion if you file a claim.

Typical duration: 12 to 24 months

For instance: Coverage starts January 1, 2024, with 12-month filing window. If you file a claim before January 1, 2025, the insurer can invoke the exclusion. If you file after January 1, 2025, they cannot.

Elimination Period (Waiting Period)

Definition: The time between when you become disabled and when benefits begin paying. This is not related to pre-existing conditions.

Typical duration: 90 to 180 days

For instance: You become disabled March 1, 2024. With a 90-day elimination period, benefits begin June 1, 2024 (if approved).

Important note: The elimination period applies to all claims, not just pre-existing conditions. This is separate from the lookback period and filing window.

Policyholder Responsibilities Relating to Pre-Existing Conditions

Policyholders have a duty to disclose their medical history accurately when applying for disability insurance. Failure to disclose pre-existing conditions may result in claim denial if those conditions lead to disability during the exclusionary period.

Contestability Period: What You Need to Know

All insurance policies contain a contestability provision, a critical issue that can affect your coverage even years after you obtain your policy.

The Two-Year Rule:

For the first two years after your policy takes effect, the insurance company can cancel your entire policy if they discover you omitted or misstated material information (significant facts that would have affected their decision to issue coverage) on your application. This applies even if the mistake was unintentional.

After Two Years:

After the contestability period expires, the insurer generally cannot cancel your policy based on application misstatements unless they prove: (1) you made the misstatement deliberately, and (2) you intended to deceive the insurance company.

What this means:

During Years 1 to 2

- Be extremely careful and thorough when completing your application

- Disclose all medical conditions, symptoms, and treatments, even if they seem minor

- If unsure whether to disclose something, err on the side of disclosure

- Keep copies of your completed application

- If the insurer questions your application accuracy, consult an attorney immediately

After Year 2

- Your coverage is much more secure

- The insurer must prove fraud to cancel your policy

- Pre-existing exclusions may still apply to specific claims, but the policy itself cannot be cancelled for good-faith errors

Seeking Legal Advice for Pre-existing Condition Exclusions in Disability Claims

When disability benefits disputes arise over the application of pre-existing condition exclusions, seeking legal advice becomes crucial. An experienced disability insurance attorney can help interpret policy language, assess the validity of a claim denial, and advocate for the policyholder’s rights.

When to Call an Attorney

You should strongly consider consulting a disability attorney if:

- Your claim was denied based on pre-existing condition exclusion, especially if the connection between past treatment and current disability seems weak

- The insurer is questioning your application accuracy, which could lead to policy rescission during the contestability period

- You are still working but considering filing a claim, and strategic timing advice could save your claim (such as waiting out the 12-month filing window)

- Your policy language is confusing or contradictory, and an attorney can identify ambiguities that work in your favor

- The insurer is using case law to support their denial, and you need an attorney who can cite counter-precedent

- Your claim involves complex medical issues, such as progressive conditions, related-but-different diagnoses, or multiple intervening events

Pre-Existing Condition Exclusions: Your Questions Answered

Does the Affordable Care Act (ACA/Obamacare) prohibit pre-existing condition exclusions in disability insurance?

No. The ACA’s prohibition on pre-existing condition exclusions applies only to health insurance. Disability insurance policies can still include pre-existing condition exclusions. This is one of the most common misconceptions.

Can the insurer deny my claim if I did not know I had the condition during the lookback period?

Generally, no. Courts have held that you cannot be treated for a condition that was not diagnosed or suspected at the time. If you saw a doctor for symptoms that later turned out to be related to a serious condition, but neither you nor your doctor suspected that condition during the lookback period, the exclusion typically does not apply. The key legal test is whether there was “concern or suspicion at that time that the observed symptoms were caused by the particular condition.

I have group disability insurance. How long do I need to work before the pre-existing exclusion does not apply?

Typically 12 months. Most group policies state that if you work continuously for 12 months (sometimes 24 months) after coverage begins, the pre-existing exclusion expires, even if you had treatment during the lookback period. This is called the “safe harbor” rule. However, you must check your specific policy as timeframes can vary. The exclusion will not apply to disabilities that occur after you complete this continuous work period.

Can my entire policy be cancelled if I forgot to mention a medical condition on my application?

It depends on timing. During the first two years after your policy takes effect (the “contestability period”), the insurer can rescind your entire policy if they discover material misstatements on your application, even if the mistake was unintentional. After two years, the insurer can only cancel your policy if they prove you made the misstatement deliberately and intended to deceive them. This is why complete and accurate disclosure on your application is critical, even for conditions that seem minor or unrelated.

The insurer says I was treated for “back pain” during the lookback period, so my herniated disc is pre-existing. Is this correct?

Not necessarily. Insurers often lump all “back problems” together. If your prior back pain was at a different spinal level, was managed conservatively with minimal intervention, and your current disc herniation represents a new injury or significant progression, you have strong arguments against the denial. Medical specificity matters. Obtain a detailed letter from your physician explaining the anatomical and clinical distinctions between the prior back pain and your current herniated disc.

I was taking medication for high blood pressure during the lookback period. Now I have had a stroke. Can they deny my claim?

No. The Meyer v. Unum decision, 2015 WL 1470447 (D. Kan. 2015), specifically addressed this issue. The court held that treating risk factors (such as high blood pressure, high cholesterol, or diabetes) is not the same as being treated for the actual disabling condition (such as stroke or heart attack). Insurers cannot lawfully treat risk factors as proxies for pre-existing conditions. If an insurer denies your claim on this basis, the denial constitutes legal overreach.

Don’t Let a Pre-Existing Condition Denial Stand Unchallenged

Pre-existing condition exclusions serve as a limited, narrow exception to coverage that insurers frequently misapply. The interpretation and application of these exclusions can become contentious, especially when the language is ambiguous or subject to multiple interpretations.

Key takeaways:

- Pre-existing does not equal pre-diagnosed. Having a past medical issue does not automatically mean your current disability is excluded.

- Treatment must be “for” the condition. Hindsight connections do not count.

- Risk factors are not conditions. Preventive care does not trigger the exclusion.

- Proximate cause matters. Insurers cannot create endless causal chains.

- Group plans have safe harbors. Working 12 months often eliminates the exclusion.

- Policy ambiguity favors you. Vague language is interpreted in your favor.

If your disability claim was denied based on a pre-existing condition exclusion, do not accept the denial at face value. Insurance companies routinely overreach, and many of these denials can be successfully challenged.

Policyholders should carefully review policy terms and seek legal guidance when faced with disability claim denials based on pre-existing condition exclusions to ensure fair treatment and proper understanding of their coverage rights.

The experienced ERISA disability attorneys at DeBofsky Law have successfully challenged pre-existing condition denials for claimants nationwide. We understand the complex interplay between medical evidence, policy language, and legal precedent, and we know how to build winning appeals.

If your disability benefits were denied due to a pre-existing condition exclusion, contact us for a consultation. We will review your denial, analyze your policy, and provide guidance on your best path forward.