When Matt Maloney tells the story of the woman who lost complete use of her arm, his voice still carries the same disbelief he felt nearly a decade ago as a young law clerk. The insurer’s response to her disability claim was as cold as it was absurd: she could still work. Just use her other arm.

“That’s when I knew how brutal these companies can be,” said Maloney, now a partner at DeBofsky Law. “And that was just the beginning.”

Over nearly ten years of practice, Maloney and the team at DeBofsky Law have seen the insurance industry’s denial playbook from every angle. The tactics are sophisticated, often hidden, and devastatingly effective. Most claimants never see them coming. They pay premiums for years, sometimes decades, believing their disability coverage will be there when they need it. Then they get sick or injured, file a claim, and discover the system isn’t designed to protect them. It’s designed to protect the insurer’s bottom line.

It’s a system that demands experienced counsel who understands how insurers operate and how to counter their strategies.

In a recent interview, Maloney pulled back the curtain on how insurers systematically deny legitimate claims, the gaps in ERISA federal law that enable this behavior, and how his firm fights back on behalf of claimants who deserve better.

The “Independent” File Reviewers

One of the most troubling tactics involves what insurers call file reviewing physicians. When you submit a disability claim or appeal, insurers routinely reach out to third-party companies who arrange for doctors to review your claim and medical records. If the claim is ultimately denied, it’s often because that doctor concluded you aren’t disabled.

Related Article: https://www.debofsky.com/articles/indepentent-medical-examination/“It’s almost as if the doctors are making these decisions because if the insurer gets that opinion that the person can work, they’re going to rely on it,” Maloney explained.

The structural conflict becomes even clearer with in-house physicians. “A pretty decent amount of insurers have their own in-house doctors who will review claims,” Maloney said. “They might say there’s no structural conflict of interest, but if the company that’s writing your checks is expecting you to behave or make an opinion a certain way, then it’s kind of hard to separate those two.”

These file reviewers often engage in what Maloney calls “cherry picking.” They selectively highlight parts of your medical records that support denial while ignoring clear evidence of disability. You might have ten appointments documenting severe limitations, but the reviewer will focus on one note mentioning a “good day” or a temporarily normal exam result.

DeBofsky Law has built its practice around recognizing and dismantling these tactics. When we review a denial, we know exactly what to look for: which physicians the insurer used, what their track records show, and how they’ve mischaracterized medical evidence. We bring in independent experts who actually understand your condition and can counter the insurer’s biased review with credible, thorough analysis.

“The selective review shows they’re not trying to understand your condition. They’re building a case against you,” Maloney said. And we’re building the case to prove them wrong.

You’re Being Watched

If the paper review doesn’t produce the denial the insurer wants, they have another card to play: surveillance.

Many claimants are shocked to learn that insurers routinely hire private investigators to stake out their homes. For days at a time, investigators watch, photograph, and record your daily activities. The goal is to capture anything that can be used against you.

Carried groceries from your car? They can claim you’re able to lift and carry items for work. Drove to a doctor’s appointment? They can argue that demonstrates an ability to sit for extended periods. Posted a vacation photo on Facebook? They can use that to suggest you’re not as disabled as you claim.

“They’ll surveil you for one, two, three days just to see what you do and where you’re going,” Maloney said. “A lot of times the claimant isn’t going anywhere because they’re unable to work.”

The surveillance is legal, but unsettling. Insurers are skilled at taking ordinary, necessary activities (going to the pharmacy, attending a child’s school event, taking a short walk) and spinning them into evidence that you’re capable of full-time work.

Social media has become another surveillance tool. Insurers monitor Facebook, Instagram, Twitter, and LinkedIn profiles, looking for any content they can use against you. A photo from a family gathering gets twisted into proof you’re social and active. Even innocent posts about hobbies can be misrepresented.

Our firm has seen every version of this tactic, and we know how to fight back. We prepare clients for the possibility of surveillance and help them understand what activities are appropriate for their health. Most importantly, we know how to contextualize surveillance footage in appeals and litigation. A 30-second video of someone walking to their mailbox doesn’t prove they can work eight hours a day, and we make sure judges and insurers understand that distinction.

The 24-Month Mental Health Trap

Perhaps the most unjust provision in disability insurance policies is the mental health limitation clause. Found in virtually every private disability policy, these clauses cap benefits for mental health conditions at just 24 months, even if your depression, anxiety, PTSD, or other condition persists for years or decades.

“They say, ‘You got your 24 months. Hopefully you’re cured now,'” Maloney said. “And once those months are used, you’re done. For life.”

If you develop severe depression that prevents you from working, you’ll receive benefits for two years. Then, regardless of your actual condition, the benefits stop. It doesn’t matter if you’re still disabled. It doesn’t matter if your doctors say you can’t work. The clock ran out.

These limitations have no basis in medical fact. Mental health conditions don’t conveniently resolve in exactly 24 months. Many are chronic, lifelong conditions requiring ongoing treatment. But insurers treat them as temporary inconveniences, not legitimate disabilities.

But DeBofsky Law isn’t just fighting these clauses in individual cases. We’re working to change the law itself. The firm is actively collaborating with Illinois state senators to ban mental health limitation clauses in policies issued in the state. It’s part of a broader advocacy effort led by founding partner Mark DeBofsky, whose legal scholarship and thought leadership have influenced ERISA law for decades.

The Discretionary Clause Problem

Buried in the fine print of many disability policies, discretionary clauses give insurers “discretion” to interpret policy terms and make benefit determinations.

That might sound reasonable until you understand what it means in court.

When you exhaust your appeals and file a lawsuit seeking benefits, the discretionary clause dramatically changes the legal standard. Instead of the court reviewing your claim fresh and making its own determination, it can only overturn the insurer’s decision if it was “unreasonable” or “arbitrary and capricious.”

“You don’t essentially get your day in court,” Maloney explained. “The court is kind of already leaning towards the insurer’s decision because of that deference.”

You’re not fighting on equal footing. The court reviews the insurer’s decision with deference rather than making its own independent determination.

About half of U.S. states have banned discretionary clauses, including Illinois. But in states where they’re still legal, insurers enjoy a massive advantage.

DeBofsky Law has built a national reputation precisely because we know how to win even when discretionary clauses apply. Our attorneys have argued precedent-setting cases in federal appellate courts, establishing legal standards that protect claimants nationwide. We’ve authored legal treatises that judges cite and taught other lawyers how to litigate these complex cases. When we take on insurers who hide behind discretionary clauses, we bring decades of specialized expertise that knows how to overcome even a deferential standard of review.

Maloney argues these clauses should be eliminated at the federal level. “Everybody would have a fair shot, regardless of what state you live in.” Until that happens, having experienced counsel who understands how to navigate these provisions can make the difference between winning and losing your case.

No Consequences, No Incentive to Change

Here’s perhaps the most frustrating reality: when insurers wrongfully deny legitimate claims, they face virtually no consequences.

The federal law governing most disability claims (the Employee Retirement Income Security Act of 1974, or ERISA) does not allow for punitive damages. If an insurer denies your claim in bad faith, drags you through years of appeals and litigation, and you finally win in court, what happens?

They pay what they already owed you. That’s it. No penalties. No meaningful interest. No damages for the emotional distress, the financial hardship, or the years of your life spent fighting.

“There’s no incentive on the insurer’s part to behave well,” Maloney said. “There’s not that threat of punitive damages.”

This creates a perverse economic incentive. From the insurer’s perspective, denying claims is essentially risk-free. Even if they lose in court, they’re only paying what they would have paid anyway. But if the claimant gives up (which many do), the insurer saves hundreds of thousands or even millions of dollars.

Most claimants don’t appeal. Of those who do, most don’t hire attorneys. Of those who hire attorneys, most settle for less than full benefits. And even those who go all the way to a favorable court decision face years of delay while battling their disability at the same time.

“Not only are you fighting with the insurance company, but you’re also dealing with a condition that’s severe enough to prevent you from working,” Maloney said. “There is a battle on two fronts.”

That’s exactly why every case at DeBofsky Law is led by an experienced attorney, not handed off to paralegals or staff. We understand that our clients are fighting for their financial survival while managing severe health conditions. They need someone who will take over the fight completely.

Our track record speaks to this commitment. With 136 five-star client testimonials and a national reputation for recovering full promised benefits, we’ve proven that insurers can be beaten, even when they think the system protects them.

What You Need to Know

Given these challenges, what should you know before filing a disability claim?

First, understand that paying premiums doesn’t guarantee benefits. You must prove you’re disabled based on how your specific policy defines “total disability,” and those definitions vary widely. Some policies require that you can’t perform “any occupation.” Others protect your specific profession. The difference can mean everything.

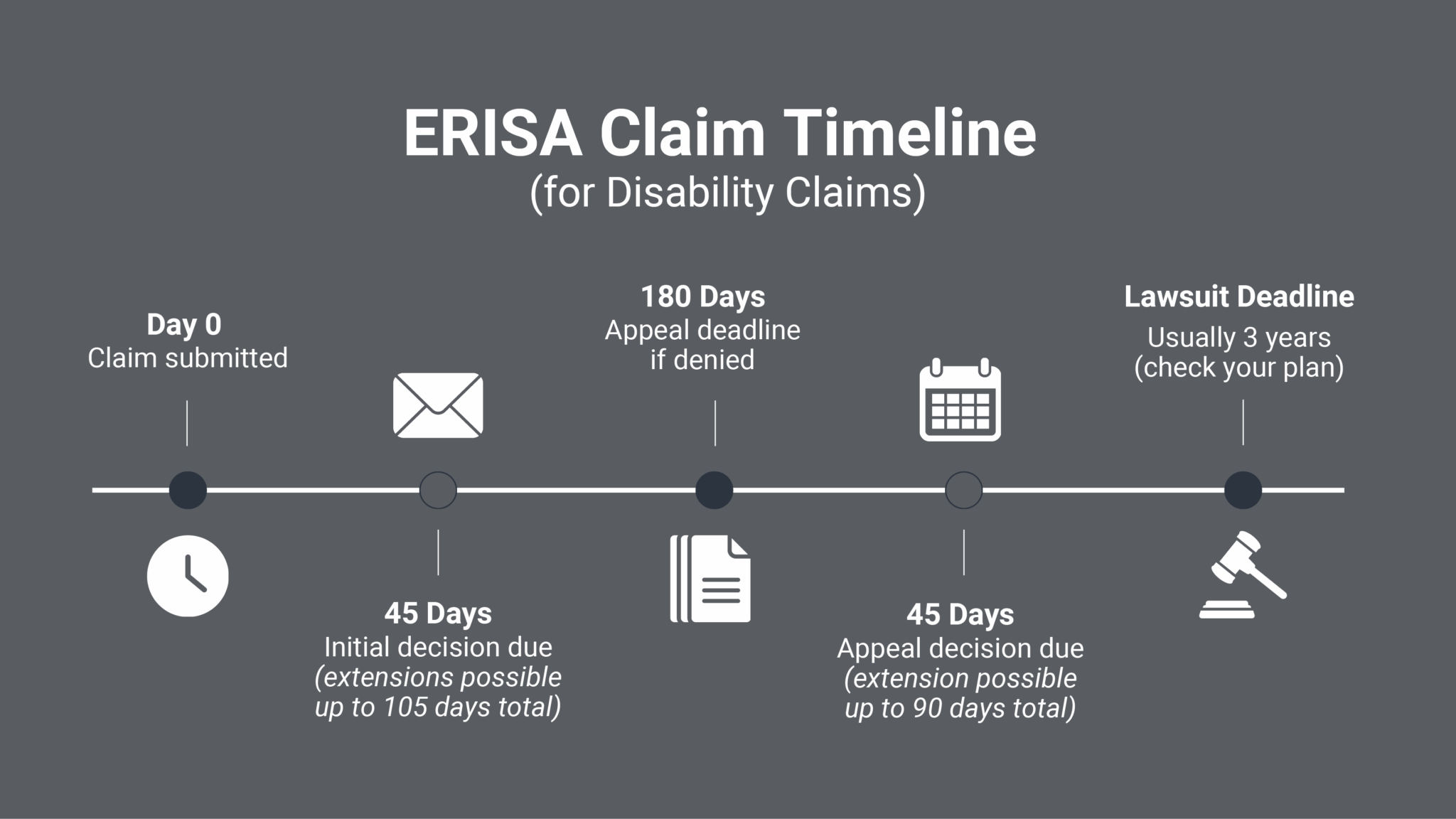

Second, the clock starts ticking the moment you receive a denial letter. You typically have just 180 days to appeal. Miss that deadline and the denial becomes final.

Related Article: Common Mistakes When Appealing a Denial of Long Term Disability BenefitsThird, documentation is everything. Your medical records, your doctors’ opinions, even the details of your job duties all matter. Incomplete or insufficient evidence is the most common legitimate reason for denials. But getting the right evidence requires knowing what the insurer needs to see and what they’ll try to use against you.

This is why Maloney urges claimants to contact a disability insurance attorney immediately, ideally before filing, but certainly within 48 hours of a denial. “That’s when I think it’s most important to contact an attorney. The earlier you’re proactive about it, the better.”

DeBofsky Law focuses exclusively on ERISA, disability, and life insurance claims. We don’t dabble in this area. It’s all we do. That specialization means we understand the insurer’s playbook because we’ve seen it hundreds of times across thousands of cases. We know which third-party reviewers are used most often and what their track records look like. We know how to counter surveillance evidence. We know how to build a record that can withstand scrutiny.

“It’s the experience,” Maloney said. “That’s what we deal with on a daily basis. We’ve seen all the tricks, we’ve seen all the tactics that insurers use.”

When you work with our firm, you’re not just getting legal representation. You’re getting advocates who will take over the entire fight so you can focus on your health, your family, and your recovery.

Why the Fight Matters

After nearly a decade of fighting these battles, Maloney hasn’t lost his sense of purpose. “Just sticking up for the little guy,” he said. “You pay into these policies over years and years, and when you need the disability benefits, you don’t get them.”

The work isn’t easy. The system is stacked against claimants. The law provides insurers with structural advantages that would be unconscionable in almost any other context. And the human toll is real: people losing their homes, draining their retirement accounts, suffering additional health declines because they can’t afford treatment, all while fighting for benefits they rightfully earned.

But there are victories. Claims that get approved. Appeals that succeed. Precedent-setting court decisions that establish protections for future claimants. Legislative progress that chips away at discriminatory policy provisions. And always, there’s the moment when an attorney at DeBofsky Law calls a client with good news.

“That’s probably the best part of my job,” Maloney said, “is getting an approval letter and calling or emailing the client to let them know. They’ll always say, ‘Thank you so much. This was a huge burden off my back.’ It’s just really nice to see that something you did really helped somebody out.”

That’s what drives everyone at DeBofsky Law: the knowledge that when insurers break the rules, we know how to hold them accountable. When they deploy their tactics, we counter with expertise, experience, and a tenacious commitment to getting our clients what they’re owed.

You paid into your policy. You deserve your benefits. And we’re here to make sure you get them.

Take Action Now

If you’re facing a disability claim denial, you don’t have to fight alone. The insurers have lawyers, doctors, investigators, and decades of experience denying claims. You deserve experienced representation that knows how to push back and win.

The clock is ticking. With only 180 days to appeal, every day matters. Contact DeBofsky Law for a consultation. We’ll review your denial, explain your options, and if we’re the right fit, take over the fight so you can focus on what matters most.

DeBofsky Law specializes exclusively in ERISA, disability, and life insurance claims litigation. Contact our team or visit our website. We’ve seen all the tricks. We know what to look for. Let us fight for you.